Table of Contents

Key Takeaways

- 01Santorini's 8,000 daily cruise passenger cap — Europe's most aggressive overtourism intervention — cut peak-day volumes by more than half and produced dramatically improved visitor experiences, but at a measured cost of -22% hotel revenue and -16% airport arrivals for 2025.

- 02The January–February earthquake swarm compounded policy impact, making it impossible to isolate the cap's standalone economic effect. The 2026 season — with earthquake fears subsided and the cap tightened — will provide the natural experiment that 2025 could not.

- 03Cruise traffic redistribution is reshaping Greek island tourism at unprecedented scale: Chania surged 43% to a record 408,946 passengers, Corfu has 562 calls booked for 2026, and new ports like Syros are entering the cruise map for the first time.

- 04The €20 peak-season cruise tax appears insufficient to alter itinerary decisions on its own — Mykonos grew 16–17% despite the same fee — suggesting the cap, not the tax, is the binding constraint driving strategic change.

- 05Cruise lines are diverging strategically: Royal Caribbean is investing in a private beach club on the island, MSC is redirecting ships to alternative ports, and the majority of premium operators are maintaining their Santorini schedules.

- 06Analysts project 20% of Mediterranean ports will introduce passenger caps or green levies by 2027, positioning Santorini as an early mover in a structural regulatory shift rather than an outlier — with implications for how the entire cruise industry plans Mediterranean itineraries.

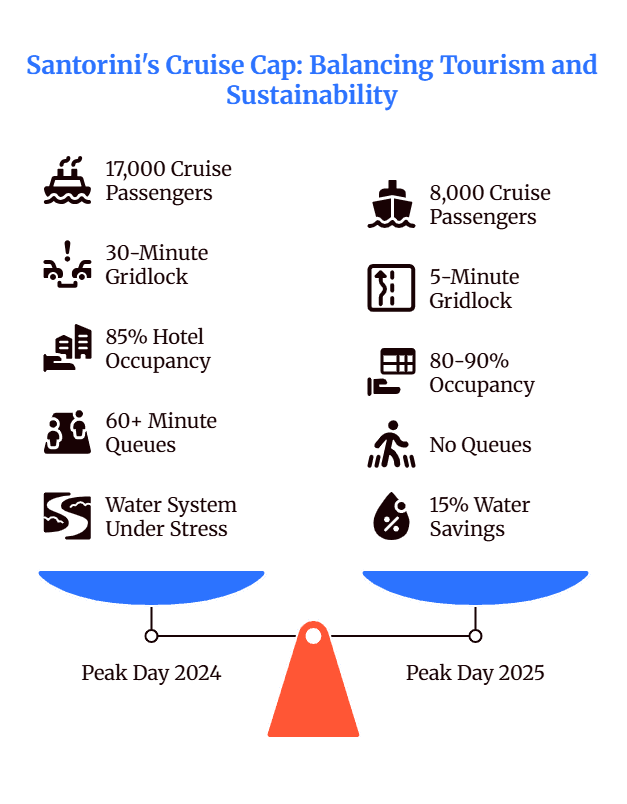

On a clear morning in July 2024, as many as 17,000 cruise passengers would arrive at Santorini's caldera port in a single day. By late morning, the cobblestone path from Fira to Oia — the island's most iconic walk — would be shoulder-to-shoulder with visitors navigating the narrow passage in a slow, unbroken stream.

The queue for a photo at Oia's famous blue-domed church could stretch past an hour. The hilltop transfer from port to village took 30 minutes in gridlock. Water pressure dropped. Waste systems strained. Locals described a place that had become, for several hours each peak-season day, unrecognizable.

One year later, the same walk is a trickle of hikers. Plunge pools in Imerovigli sit empty. A London visitor told Argophilia she reached the hilltop from the port in five minutes. And Santorini's hotel revenue has fallen 22%.

That is the paradox at the center of the most aggressive overtourism intervention in European history: the policy is working exactly as designed, and the economic cost is substantial.

What makes the story more complicated — and more instructve — is that Santorini's 2025 experience cannot be attributed solely to the cruise cap. An earthquake swarm, a new per-passenger tax, and broader airline capacity reductions all converged in the same year, making clean causal attribution impossible and the policy lessons both profound and contested.

This analysis draws on Fraport Greece airport statistics, ELSTAT revenue data, port authority records, cruise line itinerary filings, and hotel market intelligence to present the most comprehensive English-language assessment of what has happened since Santorini's daily cruise cap took effect — and what comes next as the policy tightens further in 2026.

What Santorini's 8,000-passenger cap actually means

Santorini's daily cruise passenger cap — set at 8,000 — is not a simple headcount at the port gate. It operates through a berth allocation system managed by the Santorini Municipal Port Fund, and its mechanics matter because they determine which ships call, when, and under what conditions.

The system works through a scoring algorithm that ranks cruise line applications based on multiple criteria: the number of annual calls a line commits to (rewarding consistency over one-off visits), the duration of each port call (longer stays score higher), the proportion of visits in the low season (incentivizing deseasonalization), and the line's cancellation history (penalizing unreliability). Ships are allocated berths based on their composite score until the daily cap is reached.

For context, peak days in 2023 and 2024 saw 11,000 to 17,000 cruise passengers arriving at the caldera from up to 17 ships simultaneously. The 8,000-passenger cap represented an immediate reduction of 27% to 53% depending on the day — effectively cutting the highest-volume days in half.

The cap's supporting regulations add enforcement teeth. Late cancellations incur a fee of €3 per booked passenger. Early departures without force majeure cost €2 per passenger per hour. These penalties are designed to prevent the gaming behavior that undermined voluntary restrictions elsewhere in the Mediterranean, where cruise lines would nominally commit to schedules and then deviate without consequence.

For 2026, the system tightens significantly through a technical change with substantial real-world impact: passenger loads will now be calculated at 100% occupancy rather than the 80% assumption used in 2025. A ship with 3,000-passenger capacity will count as 3,000 against the daily limit, not the 2,400 that applied under the previous formula. The practical effect is fewer ships on any given day, even with the same numerical cap — a meaningful squeeze on peak-season capacity.

The academic basis for the 8,000 figure traces to a 2018 University of the Aegean study led by Professor Lekkakou, which determined that Santorini could sustain exactly 8,000 cruise visitors per day during peak season without exceeding infrastructure carrying capacity.

That study predated the earthquake, the tax, and the post-pandemic surge in cruise ship sizes — but its central finding has held up as the operational cap has been implemented, with Port Fund President Giorgos Nomikos reporting "smooth and orderly operation in both ports" throughout the 2025 season.

The immediate impact: a tale of two halves

Santorini's 2025 tourism performance was not uniformly devastating. It was a story of two distinct halves — a brutal spring followed by partial summer stabilization — and understanding that trajectory matters for interpreting what comes next.

Full-year airport data from Fraport Greece shows Thira Airport processed 2,418,219 total passengers in 2025, down from 2,877,122 in 2024. That is a 16% full-year decline, representing approximately 459,000 fewer arrivals. But the distribution across the calendar reveals a more nuanced picture.

The first half was severe. H1 2025 airport arrivals fell 21.4% year-over-year, driven by the compounding effects of the January–February earthquake sequence, subsequent airline capacity cuts, and the forward-booking cancellations that followed both. The damage was concentrated in the months when summer bookings are made: airlines pulled seat capacity by 26%, and forward bookings dropped 23%.

The second half showed clear stabilization. H2 arrivals declined a more moderate 12.9% — still negative, but roughly half the pace of the first-half decline. The critical summer months delivered better-than-feared results: August was the best-performing month at -9.4% (465,850 passengers versus 514,055 the prior year), while July came in at -11.6%. These are meaningful declines, but they fall well short of the 20–40% full-year losses that local industry leaders had predicted during the earthquake crisis.

The shoulder season, however, disappointed. September fell -15.2% and October dropped -19.3%, suggesting that the island failed to capture the extended-season benefits that policymakers had hoped the cruise cap might enable by improving the perception of Santorini as an uncrowded destination. The shoulder months remained weaker than the summer core, not stronger.

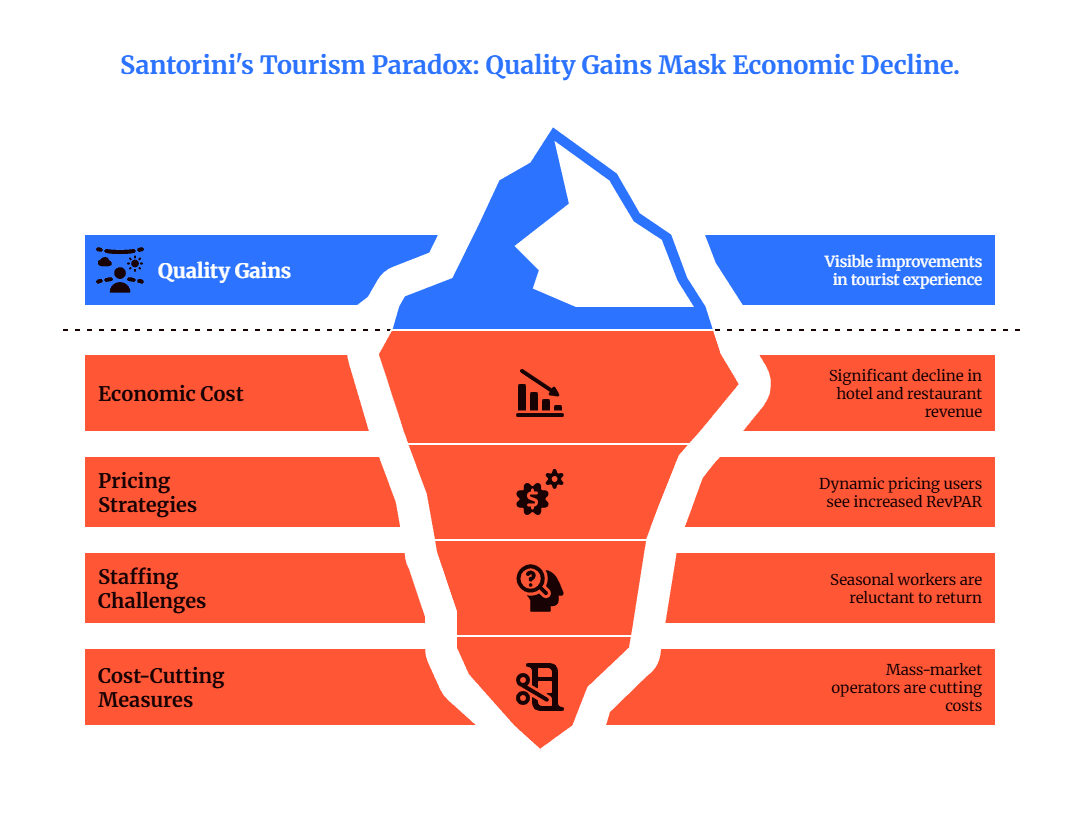

Hotel performance tracked the airport data with a revenue dimension that reveals the severity of the pricing impact. Occupancy plunged to roughly 70% in June — down from 85% the prior year — before recovering to 80–90% in July and August. Those summer occupancy figures are respectable but came at a steep price: Lighthouse Intelligence reported that Santorini summer hotel rates fell 14% year-over-year, the largest decline among all Mediterranean island destinations tracked. Hotels routinely offered 40–50% discounts off 2024 rates to fill rooms.

One hotelier, Nikos Tsolakakis, described to Greek Reporter a compounding effect: already reduced rates dropping further onto already reduced baseline prices, producing what he quantified as a cumulative "minus 60%" compared to 2023 levels.

The five-star segment fared somewhat better — HotelInsider's market analysis showed weighted average ADRs still peaking above €700 per night in early June before declining to around €500 by mid-October — but even luxury properties felt the squeeze.

The most recent official revenue data comes from ELSTAT's Q2 2025 report, which showed hotel turnover down -22.1% and restaurant revenue down -21% versus Q2 2024.

These were the steepest declines of any Greek destination during a period when the national hotel sector grew 2.6%. Q3 and Q4 revenue figures have not yet been published, but the moderating airport decline in the second half suggests the revenue picture likely improved somewhat during peak season — without fully recovering.

The earthquake confound: separating policy from seismology

Any honest assessment of the cruise cap's impact must reckon with a critical confound that makes clean attribution essentially impossible: the January–February 2025 earthquake swarm.

Beginning in late January 2025, Santorini and the surrounding Cycladic area experienced more than 20,000 tremors over several weeks. The intensity was sufficient to trigger a state of emergency declaration, close schools for a month, and impose a temporary ban on cruise ships entering the caldera port. For an island whose economy depends almost entirely on perceptions of safety and tranquility, the seismic crisis could not have been more destructively timed — it struck precisely during the January–March booking window when most summer reservations are made.

The measurable effects were immediate and severe. Forward bookings dropped 23%. Airline seat capacity was cut 26%. Viking and Celestyal cancelled or rerouted their March cruise calls. The first cruise ship did not return until March 23. SETE President Yannis Paraschis quantified the compounding damage: summer airline losses projected at 10–15% from the earthquake alone.

The recovery timeline offers some basis for disentangling the two causes. By April, accommodation bookings were picking up. Some luxury properties — notably Canaves Ena — reported May figures that exceeded the prior year, suggesting the highest-value segment recovered relatively quickly. By October 6, seismometers were barely registering activity. By February 2026, geological conditions had been calm for months, and the Santorini-View booking platform reported "a steady flow of daily bookings" for the coming summer.

But the honest conclusion is that no reliable method exists to cleanly separate earthquake-driven losses from cap-driven losses. The two operated on the same island, in the same season, on the same travelers' perceptions. Industry estimates of the earthquake's standalone impact range from 5% to 15% of the total decline — which would place the cap's isolated contribution somewhere between a modest drag and a substantial one. Both interpretations are consistent with the data.

The 2026 season will provide the natural experiment that 2025 could not: with earthquake fears fully subsided and the cap tightened further, any continued decline or recovery in arrivals will be more directly attributable to policy rather than geology.

The winners: where cruise lines redirected

The most dramatic and measurable outcome of the Santorini experiment is the redistribution of cruise traffic toward alternative Greek ports. The data here is unambiguous and, in several cases, striking in its scale.

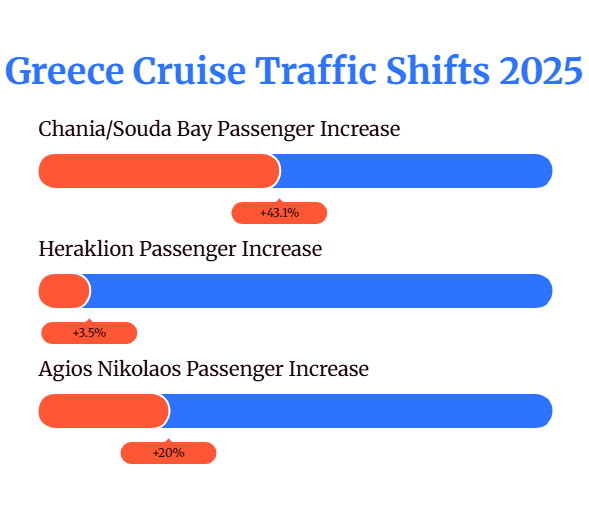

Chania (Souda Bay) on Crete recorded the most dramatic growth. The port welcomed a record 408,946 cruise passengers in 2025 — up 43.12% from 285,729 the prior year — across 204 ship calls versus 144. A team of just 12 port employees managed the entire operation.

The municipality expects over €500,000 in cruise-related fee revenue, and the port anticipates 195–220+ arrivals in 2026 with plans to develop homeporting capability. For an island that already surpassed 10 million airport passengers for the first time, the cruise surge represents an additional growth vector that positions Crete as the primary beneficiary of Santorini's constraints.

Corfu has established itself as a year-round cruise hub with 562 confirmed calls for 2026 — a 20.3% increase — and forecast passenger volumes approaching one million (998,244 projected). Port Authority CEO Dimitris Apergis described it as "a clear strategy to strengthen its international position." The January-to-March 2026 period alone has 36 calls scheduled, up from 31, signaling meaningful winter cruise activity that most Greek ports have never achieved. With tourism already contributing more than 90% of Corfu's local GDP, the cruise expansion deepens both opportunity and dependency.

Piraeus set records with approximately 1.85 million cruise passengers in 2025, cementing its position as the eastern Mediterranean's dominant cruise hub and the natural gateway for Athens-based itineraries.

Several smaller ports are growing from modest bases with notable momentum:

Heraklion handled 536,543 passengers across 281 calls in 2025, a 3.5% increase that reflects steady rather than dramatic growth from Crete's established cruise infrastructure.

Volos surpassed its best performance of the past decade by September, hosting 25 ships and 39,758 passengers — a signal that mainland ports are entering cruise itineraries that previously defaulted to island calls.

Agios Nikolaos grew 20% in 2025 and expects over 40% growth in 2026, with Celestyal committing to weekly visits and plans for VIP homeporting services. The eastern Crete port offers proximity to attractions like Spinalonga and the Elounda luxury hotel corridor — including the forthcoming Rosewood Blue Palace — creating a natural cruise-to-luxury pipeline.

Syros is entering the cruise map for the first time in 2026 as MSC Cruises' chosen alternative to Santorini. MSC has described Ermoupoli's neoclassical harbor and the medieval village of Ano Syros as a "hidden gem" — precisely the kind of authentic, uncrowded experience that the Santorini cap was partly designed to redirect visitors toward.

The pattern reveals something more significant than simple displacement. Greece's total cruise sector grew to approximately 8 million+ passengers nationally in 2025, suggesting that the redistribution is not a zero-sum game where alternative ports merely absorbed Santorini's losses. New capacity is being added across the archipelago, and the cruise industry's overall Mediterranean footprint continues to expand.

The question is whether ports like Chania and Agios Nikolaos can sustain double-digit growth without eventually facing the same congestion pressures that prompted Santorini's intervention — a question that, for now, remains theoretical given the dramatically larger land area and infrastructure capacity of destinations like Crete.

Thessaloniki presents a more complex case. The port hosted 71 cruise calls in 2025 with 20 different ships from 14 companies, including noteworthy first-time visitors like Viking Star, Astoria Grande, Emerald Cruises, and the Ritz Carlton yacht. Crystal Cruises even used the city as a homeport. But Celestyal Cruises — described as "the backbone keeping the city's cruise activity alive" — has removed Thessaloniki from its 2026 itineraries, potentially cutting calls to as few as 40. Viking is partially compensating with 9 planned calls (up from 4), and Celebrity Infinity has 23 scheduled.

The city is simultaneously completing a €195.6 million Pier 6 expansion signed in November 2025, betting that infrastructure investment will attract the traffic that Celestyal's departure temporarily removes.

Mykonos offers an instructive contrast. Despite the identical €20 peak-season cruise tax, the island projected approximately 900 cruise calls and 1.5 million+ passengers for 2025 — growth of roughly 17% in calls and 16% in passengers over 2024. Mykonos implemented the same berth allocation system but no hard daily cap, and cruise lines appear to have absorbed the tax without meaningfully altering itineraries.

The Mykonos Port Fund President publicly opposed the tax, calling it "a curse for the island," but the numbers tell a different story — suggesting that the cap, not the tax, is the binding constraint driving strategic change.

The quality argument: fewer visitors, better experience

The economic data tells one story. The on-the-ground experience tells another — and for Santorini's long-term positioning, it may be the more important one.

With the 8,000 daily cap in place and enforced, the operational transformation was immediately visible. Port Fund President Nomikos reported "smooth and orderly operation in both ports" with passenger flows "without congestion."

The cap held at 8,000 throughout the season, with only rare exceptions reaching 9,000. These are not subjective impressions — they represent a fundamental change in the daily rhythm of an island that had been operating well beyond its carrying capacity.

Visitor reports from the 2025 season consistently describe a place that felt, for the first time in years, like a destination rather than a bottleneck. No queues at Oia's iconic blue-dome photo spots. A "small trickle of hikers" on the Fira-to-Oia path rather than the previous wall-to-wall procession. Port-to-hilltop transfers completed in five minutes instead of 30. These improvements matter for the premium positioning that Santorini depends on — a €700-per-night hotel loses its value proposition when the experience outside its door involves gridlock and hour-long queues.

The water data reinforces the infrastructure argument. Reports of a 15% reduction in water consumption during the capped season suggest that the daily population load was meaningfully lower — a significant consideration for an island that imports much of its fresh water by tanker and desalination.

The luxury segment's resilience provides perhaps the strongest evidence that quality-over-quantity economics can work. Canaves Ena's general manager, Giannis Bubaris, reported that May 2025 figures exceeded May 2024, calling the reduced crowds "a great opportunity for someone who wants to visit Santorini." Hotels that employed dynamic pricing tools saw +25% RevPAR gains over the prior year, according to HotelLab data.

This represents a self-selected sample of the most sophisticated operators, but it demonstrates that technology-enabled, premium-focused properties can thrive in a constrained environment — even as the broader market contracts.

Mayor Nikos Zorzos has reinforced the quality thesis from a governance perspective, declaring "Santorini does not need any more beds" and freezing new hotel construction. Public investment is being redirected toward cliff stabilization, port upgrades, and emergency response systems — infrastructure that serves the existing visitor base rather than expanding the island's capacity to absorb more.

The counterargument — voiced by mass-market operators who have seen revenue decline by 20% or more — is that the quality improvement benefits a narrow luxury segment while the broader economic ecosystem that depends on volume (tour operators, budget restaurants, transport services, seasonal workers) bears the cost. Hotelier Nikos Tsolakakis described cutting "employees, energy, food, services — everything so that we can survive." Fyralia Hotel manager Christina Dimopoulou confirmed being "definitely in a decline." One unnamed hotel owner called it "a crisis unprecedented in its nature" that would "take years to rebuild the image of the island."

This tension — between a genuinely improved visitor experience and genuine economic pain — is the central dilemma that any overtourism intervention must navigate. Santorini's data from 2025 suggests that both narratives are simultaneously true.

The cruise tax: €20 per passenger and what it costs a family

Greece's Sustainable Tourism Fee for Cruise Passengers, introduced in July 2025, created the most aggressive per-head cruise tax system in the Mediterranean. The tiered structure charges by destination and season:

Santorini and Mykonos (the two highest-impact ports): €20 per passenger during peak season (June through September), dropping to €12 in the shoulder months and €4 in winter. All other Greek ports: €5 in peak season, €3 in shoulder months, and €1 in winter.

For a family of four visiting Santorini as part of a peak-season cruise, the fee adds €80 to the cost of that single port call. A week-long Greek island cruise with stops at Santorini, Mykonos, and two other ports would add approximately €130 in port fees for a couple — meaningful but not prohibitive relative to the typical cost of a Mediterranean cruise.

The revenue implications are substantial at national scale. Based on 2024 passenger volumes, the tax is projected to generate €50–100 million annually across all Greek ports. The funds are earmarked for port infrastructure, environmental mitigation, and municipal services in affected communities.

Collection is handled through a centralized digital platform operated by the Ministry of Shipping, with cruise lines absorbing and passing through the charges via onboard account debits.

The Mykonos comparison is revealing. Despite the same €20 peak-season fee, Mykonos cruise traffic grew 16–17% in 2025 — indicating that the tax alone, without a daily cap, is insufficient to alter cruise line itinerary decisions. Lines appear to be absorbing the cost as a routine port expense, much as they do with berthing fees and port agent charges throughout the Mediterranean.

This suggests the cap — not the tax — is the primary policy lever driving behavioral change in how cruise lines allocate their ships.

No legal challenges to either the cap or the tax have been filed. No rate adjustments for 2026 have been announced. CLIA, the cruise industry's primary trade body, has adopted a cooperative stance, committing to a joint working group with the Greek government while pointedly noting that cruise passengers represent only 4.5% of Greece's 40 million+ annual visitors — a framing designed to push back against what it perceives as disproportionate regulatory focus on the cruise sector.

For travelers planning a Greek islands cruise, the practical takeaway is straightforward: budget an additional €20 per person for any Santorini or Mykonos stop during June–September, and significantly less for shoulder-season or winter cruises calling at other Greek ports.

Cruise lines that have invested heavily in Greek itineraries — including Royal Caribbean, Celebrity, and the luxury operators — have not raised fares specifically to offset the tax, though broader fare increases across the industry make precise attribution difficult.

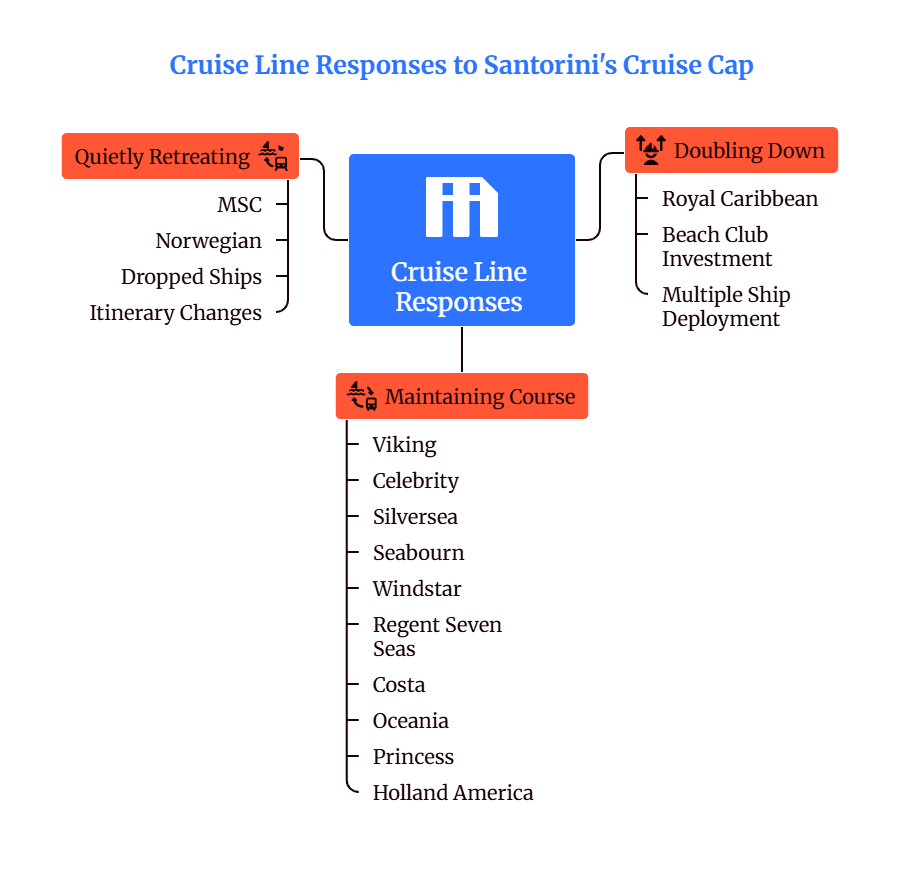

How cruise lines are responding: doubling down or quietly retreating

The cruise industry's strategic response to Santorini's restrictions has produced a fascinating divergence — a spectrum running from aggressive investment to quiet withdrawal — that reveals how different operators are reading the future of capped Mediterranean destinations.

Royal Caribbean is making the boldest bet. The line will open Royal Beach Club Santorini at Vlychada in summer 2026 — its first private beach club destination anywhere in Europe. The facility is explicitly designed to redistribute visitors across three starting points: traditional village visits to Oia or Fira, and the beach club itself.

Priced at roughly $284 per adult, it signals Royal Caribbean's conviction that Santorini remains worth significant capital investment despite the restrictions. Ships from both Royal Caribbean International and Celebrity Cruises will have access, with Odyssey of the Seas, Brilliance of the Seas, and multiple other vessels scheduled. The strategy — creating proprietary onshore infrastructure that controls the visitor experience within a capped environment — may represent a template for how major cruise lines adapt to capacity-restricted destinations globally.

MSC Cruises has moved most visibly in the opposite direction. MSC Lirica and MSC Divina will both skip Santorini in 2026, replacing the island with the new port of Syros (described as a "hidden gem" with its neoclassical Ermoupoli harbor and medieval Ano Syros hilltop) and Marmaris on the Turkish coast. Only MSC Sinfonia continues to call at Santorini.

The decision reflects a straightforward commercial calculation: for a volume-focused operator running large ships, the tighter 100% occupancy rule for 2026 makes berth allocation more difficult and potentially less profitable than redirecting to ports with no caps and lower fees.

Norwegian Cruise Line dropped Santorini from its May 10, 2026 Pearl sailing, replacing it with Mykonos and citing "revised port availability" — almost certainly a direct consequence of the tightened berth allocation system.

The vast majority of operators, however, are maintaining their Santorini itineraries. Viking, Celebrity, Silversea, Seabourn, Windstar, Regent Seven Seas, Costa, Oceania, Princess, Holland America, Azamara, Disney, and Crystal all have ships scheduled for Santorini calls in 2026. Celestyal Cruises CEO Chris Theophilides confirmed: "Our 2026 and 2027 Greece itineraries are already in place with no planned changes." The island's status as what Nomikos calls an irreplaceable part of "no Aegean cruise itinerary" appears to hold — for now.

The pattern across these decisions is consistent with industry scale. The lines retreating are primarily high-volume, mass-market operators (MSC, Norwegian) whose largest ships face the tightest squeeze under the 100% occupancy rule.

The lines maintaining or investing are premium and luxury operators (Viking, Silversea, Seabourn, Crystal, Regent) whose smaller ships and higher per-passenger spending align more naturally with a capped environment — plus Royal Caribbean, which is choosing to invest its way into compliance rather than retreat.

Carnival CEO Josh Weinstein summarized the industry's broader view: "I don't expect anything incredibly disruptive. Unfortunately for us, this is just par for the course." He cited Dubrovnik's cruise management experience as a precedent — a destination that implemented caps and taxes several years ago and remains a standard feature of Mediterranean itineraries despite the restrictions.

Ripple effects: will other destinations follow?

Santorini is not implementing cruise restrictions in isolation. It is an early — arguably the most aggressive — mover in a Mediterranean-wide regulatory trend that analysts project will accelerate significantly through the end of the decade.

Cannes voted in June 2025 to admit only ships of 1,000 passengers or fewer starting January 2026, effectively banning all major cruise ships from the French Riviera port. The city also imposed a 6,000 daily visitor cap.

Palma de Mallorca negotiated a CLIA agreement limiting the port to 3 cruise ships per day — a softer approach than a passenger cap but one that still constrains peak-day volumes.

Dubrovnik — the original cruise restriction pioneer — maintains a cap of 4,000 simultaneous visitors in the Old Town, a limit that has been in place for several years and has become an accepted feature of the port's operations.

Industry analysts at WeOnCruise project that 20% of Mediterranean ports will introduce some form of passenger cap or green levy by 2027, up from approximately 5% today. If that projection holds, the Santorini model — scoring algorithm, daily cap, sliding-scale taxation — could become the default regulatory framework for high-pressure destinations across the region.

Within Greece, the immediate question is whether Mykonos will adopt a hard cap. The island implemented the same €20 cruise tax and the berth allocation system, but stopped short of a daily passenger ceiling. Cruise traffic grew 16–17% in 2025 despite the tax — a data point that could argue either direction. Growth advocates will cite it as evidence that the tax is sufficient management without a cap. Sustainability advocates will argue it demonstrates that taxation alone is inadequate to constrain volume.

Rhodes, which delivered its best tourism season ever in 2024 after the devastating 2023 wildfires, is watching the Santorini experiment from a position of strength but is not currently pursuing caps. Greece's planned Tourism White Paper 2030–2035, expected later in 2026, will likely formalize the strategic framework — and may establish criteria for when and how additional destinations could adopt caps.

The Mediterranean context matters for travelers comparing Greek island options. The regulatory divergence between destinations — capped Santorini versus uncapped Mykonos, high-fee Cyclades versus low-fee Dodecanese — creates genuinely different visitor experiences that are now policy-determined, not just geography-determined.

A cruise itinerary that includes Santorini in 2026 will have a qualitatively different port experience than the same ship's stop at an uncapped destination like Rhodes or Heraklion.

What this means for travelers

For visitors planning a trip to Santorini or evaluating Greek island cruise itineraries, the data from 2025 carries several practical implications.

The visitor experience has genuinely improved. If the primary concern is crowd levels, 2025 and 2026 represent the best years to visit Santorini in at least a decade. Peak-day cruise volumes have been cut by more than half, queues at signature viewpoints have disappeared, and the island's infrastructure is operating within its designed capacity for the first time in years. Travelers who avoided Santorini because of overtourism reports should reconsider.

Prices are significantly lower — for now. The 14% summer rate decline and 40–50% discounts reported across the hotel market represent genuine savings for travelers booking in the 2025–2026 window.

Five-star properties that commanded €700+ per night in early summer have been available at €500 by mid-autumn. Whether these discounted rates persist into 2027 and beyond depends on whether arrivals recover as earthquake fears fully dissipate — but for the immediate booking window, Santorini is offering better value than at any point since before the pandemic.

Cruise itineraries are diversifying. The redistribution of cruise traffic toward Chania, Corfu, and emerging ports like Agios Nikolaos and Syros means that Greek cruise itineraries are becoming more varied. Travelers who previously had limited options beyond the standard Athens–Mykonos–Santorini circuit now have access to itineraries that include Crete's western coast, the Ionian islands, and mainland ports.

For those weighing whether to visit Crete as an alternative, the island's record-breaking 2025 cruise season — and its dramatically larger land area — suggests it can absorb growing visitor numbers without the congestion that constrained Santorini.

Shoulder-season economics favor independent travelers over cruise passengers. The sliding cruise tax — from €20 in peak season to €4 in winter — creates a financial incentive to visit outside June–September.

Combined with the Climate Resilience Fee reduction (from up to €15 per night to as little as €3 at 4-star hotels outside peak season) and generally lower accommodation rates, the total cost of an October or May Santorini visit could be 40–50% lower than a July equivalent — with a comparable or superior experience given the reduced crowds.

For travelers planning a broader Greek itinerary, building Santorini into a shoulder-season visit rather than a peak-summer one now has both experiential and financial logic.

The 2026 cap tightening means peak-season cruise spots will be more limited. The shift to 100% occupancy assumptions for the daily cap calculation means fewer ships on any given day.

Travelers who specifically want the cruise experience at Santorini should book with lines that have strong allocation scores — Royal Caribbean, Celebrity, and the luxury operators that the algorithm rewards for consistency, longer calls, and clean cancellation records.

What this means for the industry

For tour operators, cruise lines, accommodation providers, and the broader Greek tourism ecosystem, the Santorini experiment carries implications that extend well beyond a single island.

Portfolio diversification is now imperative. The data from Chania (+43%), Corfu (562 calls booked for 2026), and emerging ports like Syros and Agios Nikolaos demonstrates that cruise demand is elastic to alternative destinations when constraints force reallocation. Tour operators and transfer companies that concentrated their business on Santorini face the most acute exposure.

Those that diversified across multiple ports — or positioned early in growing destinations like western Crete — are capturing the redistributed volume. The lesson for the broader Greek tourism industry is structural, not cyclical: policy-driven capacity constraints are likely to expand, and businesses anchored to a single high-volume destination carry regulatory risk that did not exist five years ago.

The premium segment is more resilient than the mass market. Luxury operators — Canaves, the dynamic pricing hotels, the five-star properties — showed significantly more resilience than mid-range and budget accommodations.

This is consistent with the broader premiumization trend visible across Greek tourism, where revenue growth has outpaced arrival growth for three consecutive years. Operators that invest in yield management, property quality, and high-value guest acquisition are better positioned to navigate a capped environment than those dependent on volume.

Cruise line strategic responses will reshape itinerary patterns. Royal Caribbean's Beach Club investment and MSC's withdrawal represent opposite endpoints of a strategic spectrum that will determine which lines serve which ports over the coming decade.

The berth allocation algorithm — which rewards consistent annual calls, longer stays, off-season visits, and reliable scheduling — creates structural advantages for operators willing to make multi-year commitments to Greek ports. Lines that treat Greek destinations as interchangeable stops will find themselves progressively deprioritized.

The regulatory trend will intensify, not recede. CLIA's cooperative posture, the absence of legal challenges, the Greek government's decision to tighten rather than soften the 2026 rules, and the broader Mediterranean trend toward caps and levies all point in one direction.

Truist Securities analyst Patrick Scholes called the restrictions "clearly not a positive" but warned it was "much too early to precisely financially quantify" the impact, estimating major cruise lines carry 5–14% Eastern Mediterranean exposure.

Bernstein maintained its positive cruise stock outlook, viewing the restrictions as manageable against industry supply growth decelerating to 4% in 2026 from 6% in 2025. The Wall Street consensus — manageable disruption, not existential threat — is likely correct for the global cruise industry, but for individual destinations and the businesses that depend on them, the effects are far more concentrated.

Two 2025 academic papers from the National Technical University of Athens provide the intellectual framework for what comes next. Lagarias, Stratigea, and Theodora, publishing in ISPRS International Journal of Geo-Information, found Santorini "confronted with severe overtourism impacts" that are "highly affecting its identity, productive model and spatial pattern, while endangering its natural and cultural wealth." Leka et al., in the journal Land, described overtourism combined with insularity and climate change as creating "a 'red code' for insular regions that calls for immediate policy action."

These are not polemics — they are peer-reviewed findings that will inform Greece's Tourism White Paper 2030–2035 and, by extension, the regulatory framework for the next decade.

Methodology and data sources

This analysis synthesizes official statistical releases, port authority records, cruise line itinerary filings, hotel market intelligence, and academic research to assess the impact of Santorini's cruise passenger cap and related policy measures across the 2024–2026 period.

Airport and arrivals data: Fraport Greece monthly passenger statistics for Thira (Santorini) Airport, covering full-year 2024 and 2025 with monthly breakdowns.

Revenue and accommodation data: ELSTAT (Hellenic Statistical Authority) quarterly revenue reports for Q2 2025; Lighthouse Intelligence Mediterranean hotel rate analysis; HotelInsider five-star market analysis; HotelLab dynamic pricing performance data.

Cruise and port data: Santorini Municipal Port Fund operational reports; individual port authority statements from Chania, Corfu, Piraeus, Heraklion, Volos, Agios Nikolaos, and Thessaloniki; Hellenic Ports Association aggregate statistics; CLIA official statements and action plans.

Cruise line data: Press releases and itinerary filings from Royal Caribbean Group, MSC Cruises, Norwegian Cruise Line Holdings, Celestyal Cruises, Viking, and individual brand schedules for the 2026 season.

Policy and regulatory data: Greek Ministry of Shipping cruise tax implementation framework; Santorini Municipal Port Fund berth allocation algorithm documentation; Greek government announcements regarding 2026 cap modifications.

Academic sources: Lagarias, Stratigea, and Theodora (2025), ISPRS International Journal of Geo-Information; Leka et al. (2025), Land journal; University of the Aegean (2018), Professor Lekkakou carrying capacity study.

Financial analysis: Truist Securities and Bernstein analyst reports on cruise industry Mediterranean exposure; Carnival Corporation earnings call commentary.

Industry context: WeOnCruise Mediterranean port regulation projections; Seatrade Cruise News and Cruise Critic industry reporting; CruiseMapper itinerary tracking data.

All currency figures are in euros unless otherwise stated. Where full-year data was not available at publication, the analysis specifies the period covered. Hotel performance metrics reflect reported figures from industry sources and may not capture the full range of property types. Cruise passenger projections for 2026 are based on confirmed bookings and schedules as of early 2026, subject to revision.

Data Sources

Data period: 2024–2026

Airport Monthly Passenger Statistics 2024–2025

Hellenic Statistical Authority Quarterly Revenue Reports Q2 2025

Santorini Municipal Port Fund

Mediterranean Hotel Rate Analysis 2025

Santorini Five-Star Market Analysis 2025

Chania, Corfu, Piraeus, Heraklion, Volos, Agios Nikolaos, Thessaloniki — individual traffic reports

Industry Statements and Five-Pillar Action Plan

Royal Caribbean Group, MSC Cruises, Norwegian Cruise Line Holdings, Celestyal Cruises, Viking — press releases and itinerary filings

Santorini Carrying Capacity Study (Professor Lekkakou)

Lagarias et al., ISPRS; Leka et al., Land journal

Methodology

This analysis synthesizes official statistical releases, port authority records, cruise line itinerary filings, hotel market intelligence, and academic research to assess the impact of Santorini's cruise passenger cap and related policy measures across the 2024–2026 period. Airport and arrivals data: Fraport Greece monthly passenger statistics for Thira (Santorini) Airport, covering full-year 2024 and 2025 with monthly breakdowns. Revenue and accommodation data: ELSTAT (Hellenic Statistical Authority) quarterly revenue reports for Q2 2025; Lighthouse Intelligence Mediterranean hotel rate analysis; HotelInsider five-star market analysis; HotelLab dynamic pricing performance data. Cruise and port data: Santorini Municipal Port Fund operational reports; individual port authority statements from Chania, Corfu, Piraeus, Heraklion, Volos, Agios Nikolaos, and Thessaloniki; Hellenic Ports Association aggregate statistics; CLIA official statements and action plans. Cruise line data: Press releases and itinerary filings from Royal Caribbean Group, MSC Cruises, Norwegian Cruise Line Holdings, Celestyal Cruises, Viking, and individual brand schedules for the 2026 season. Policy and regulatory data: Greek Ministry of Shipping cruise tax implementation framework; Santorini Municipal Port Fund berth allocation algorithm documentation; Greek government announcements regarding 2026 cap modifications. Academic sources: Lagarias, Stratigea, and Theodora (2025), ISPRS International Journal of Geo-Information; Leka et al. (2025), Land journal; University of the Aegean (2018), Professor Lekkakou carrying capacity study. Financial analysis: Truist Securities and Bernstein analyst reports on cruise industry Mediterranean exposure; Carnival Corporation earnings call commentary. Industry context: WeOnCruise Mediterranean port regulation projections; Seatrade Cruise News and Cruise Critic industry reporting; CruiseMapper itinerary tracking data. All currency figures are in euros unless otherwise stated. Where full-year data was not available at publication, the analysis specifies the period covered. Hotel performance metrics reflect reported figures from industry sources and may not capture the full range of property types. Cruise passenger projections for 2026 are based on confirmed bookings and schedules as of early 2026, subject to revision.

The Greek Trip Planner research team analyzes tourism data, government statistics, and industry reports to provide actionable insights for travelers and travel professionals.