Table of Contents

Key Takeaways

- 01Greece's tourism revenue reached €22.38 billion through October 2025 — already exceeding the full-year 2024 total — with revenue growth (+8.9%) running at double the rate of arrival growth (+4.4%).

- 02Average visitor spending rose to €602.20 per trip, but average stay length has dropped 35% since 2019 (from 7.4 to 4.7 nights), signaling a fundamental shift toward shorter, higher-intensity visits.

- 03The UK emerged as 2025's breakout market with €3.55 billion in receipts (+15.1%), nearly closing the gap with Germany, while US visitors averaged €958.66 per trip — 59% above the overall average.

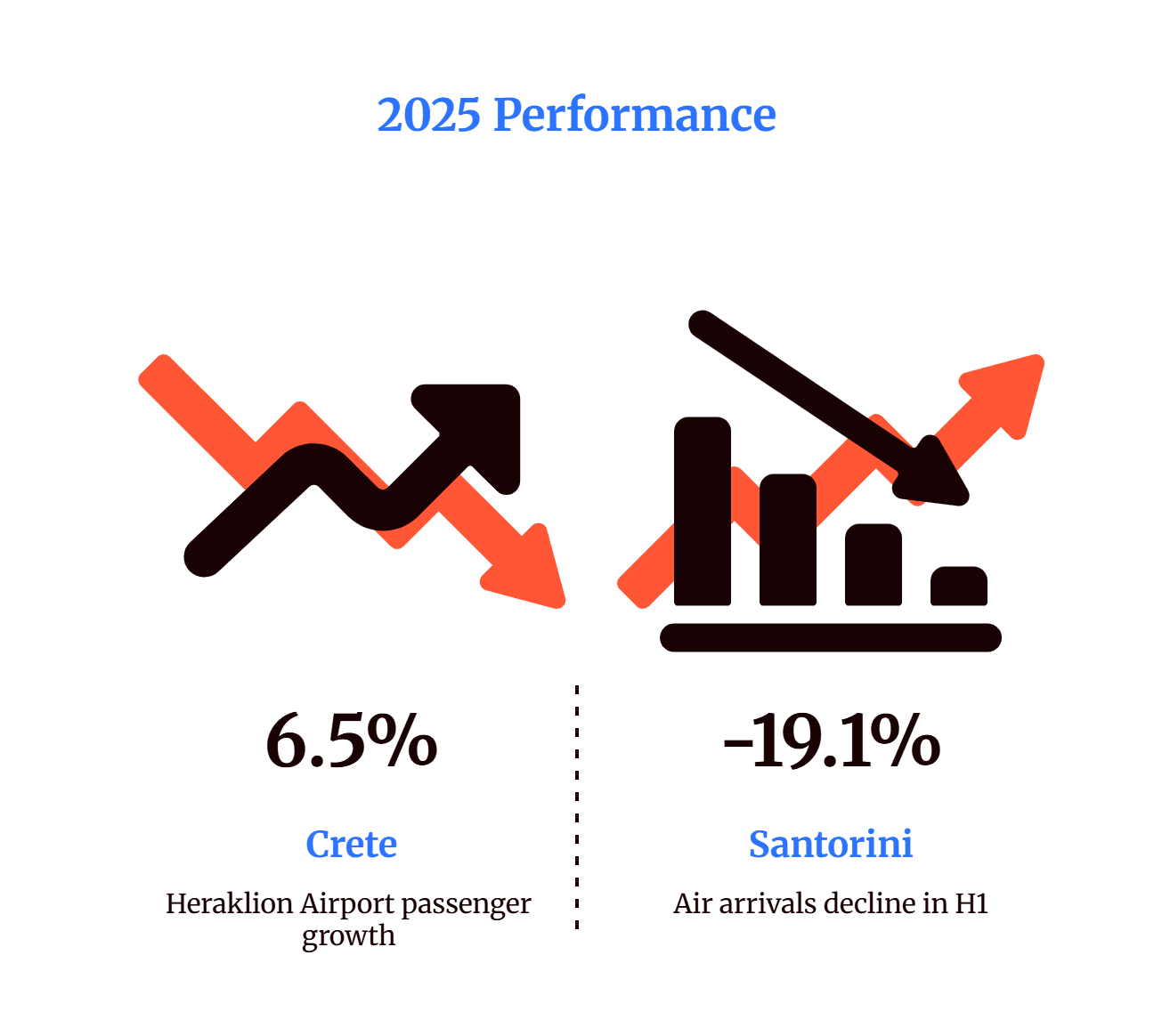

- 04Crete's Heraklion Airport surpassed 10 million passengers for the first time, while Santorini's air arrivals fell 19.1% in the first half — a stark divergence driven by cruise caps, earthquakes, and structural market shifts.

- 05New sustainability fees — including €20 cruise passenger taxes and €15/night accommodation levies at 5-star hotels — are actively reshaping travel patterns toward shoulder seasons and alternative destinations.

- 06Greece is targeting 50 million visitors and €27 billion in revenue by 2030, backed by €12+ billion in tourism investment since 2022 and 60+ hotel projects opening by 2027.

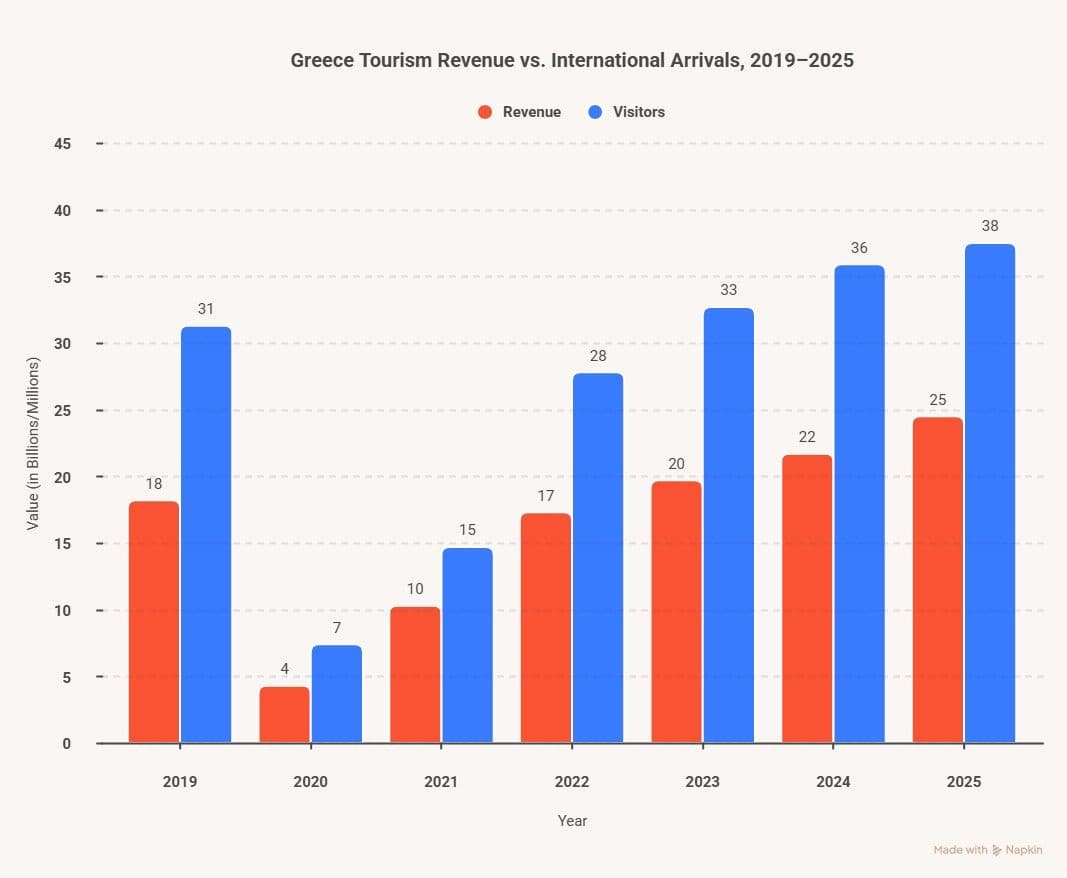

Greece broke its own tourism records in 2025: 37.98 million international visitors and €22.4 billion in revenue (Bank of Greece data, full-year). Arrivals grew 5.6% over a record 2024 — but the more important figure is the gap between volume and value. Revenue grew nearly twice as fast as arrivals (+8.9% vs +4.4%), the clearest signal yet that Greek tourism is undergoing a structural shift toward shorter, higher-spend visits.

This analysis draws on Bank of Greece travel statistics, INSETE statistical bulletins, Fraport traffic reports, and individual port authority records to track where Greek tourism actually went in 2025 — and where it's heading in 2026.

The revenue picture: €22.38 billion and counting

The Bank of Greece reported tourism receipts of €22.38 billion for January through October 2025, an 8.9% increase over the same period in 2024. The growth trajectory was particularly strong in the first half, when revenue surged 11% to reach €7.6 billion. By August, cumulative receipts had climbed to €16.7 billion — a 12% increase that reflected both rising visitor numbers and meaningfully higher per-capita spending.

The travel balance surplus — tourism receipts minus what Greeks spend abroad — exceeded €19 billion through October. That figure alone covers roughly two-thirds of Greece's goods trade deficit, underscoring just how central tourism remains to the country's macroeconomic stability.

What's driving the revenue outperformance? Two factors stand out.

First, non-EU markets are contributing disproportionately. Receipts from visitors outside the European Union grew 12.2% to reach €9.11 billion, compared with a 5.8% increase from EU-27 sources (€12.12 billion). This gap reflects Greece's growing success in attracting long-haul travelers — particularly from the United States, where receipts reached €1.54 billion through October, an 8.4% increase — who tend to spend considerably more per trip.

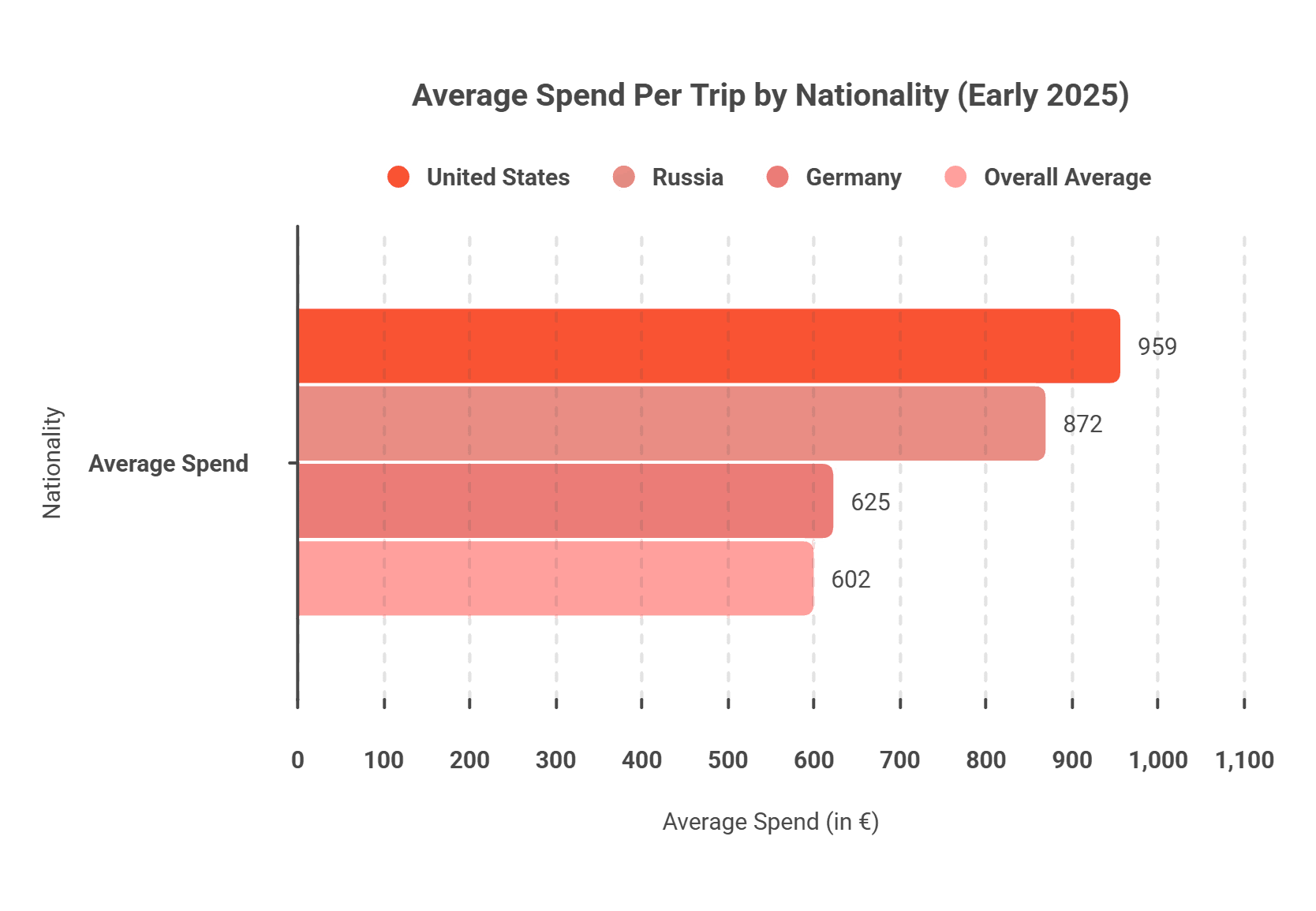

Second, average expenditure per visitor rose to €602.20, a 3.9% increase that masks enormous variation by nationality. American visitors averaged €958.66 per trip in early 2025 — 59% above the overall mean. German travelers, Greece's largest source market by volume, averaged €625.04. The premium attached to long-haul visitors helps explain why the government and industry are investing heavily in new direct air connections to the US, UK, and — for the first time in 2026 — India.

Shorter stays, bigger wallets: the new visitor profile

One of the most consequential shifts in Greek tourism is the ongoing compression of average stay length. Visitors spent 4.7 to 4.9 nights in Greece during the 2025 peak season (July–August), down from 5.9 nights in 2024 and 7.4 nights in 2019. That's a 35% reduction in six years.

The pattern is clear: travelers are visiting Greece more frequently but for shorter periods, and they're spending more intensely during those compressed windows. Higher daily spend is more than compensating for fewer nights, resulting in net revenue growth per visitor. But the shift carries operational implications that ripple through the entire hospitality chain — from how hotels price short stays to how tour operators structure multi-day itineraries.

August 2025 recorded 33.94 million overnight stays, a 2.9% increase year-over-year, with international guests accounting for 76.5% of arrivals and 83.8% of overnight stays. The gap between those two percentages tells its own story: international visitors stay longer than domestic ones, making them disproportionately valuable to the accommodation sector.

For travelers planning a trip to Greece, the data suggests that the old model of two-week Mediterranean holidays is giving way to more focused visits — often a week or less — built around specific islands, cities, or experiences. Budget-conscious visitors wondering how much a Greece trip costs should note that while stays are getting shorter, daily costs at upper-tier properties have increased materially, partly driven by new accommodation taxes.

Source markets: the UK's breakout year

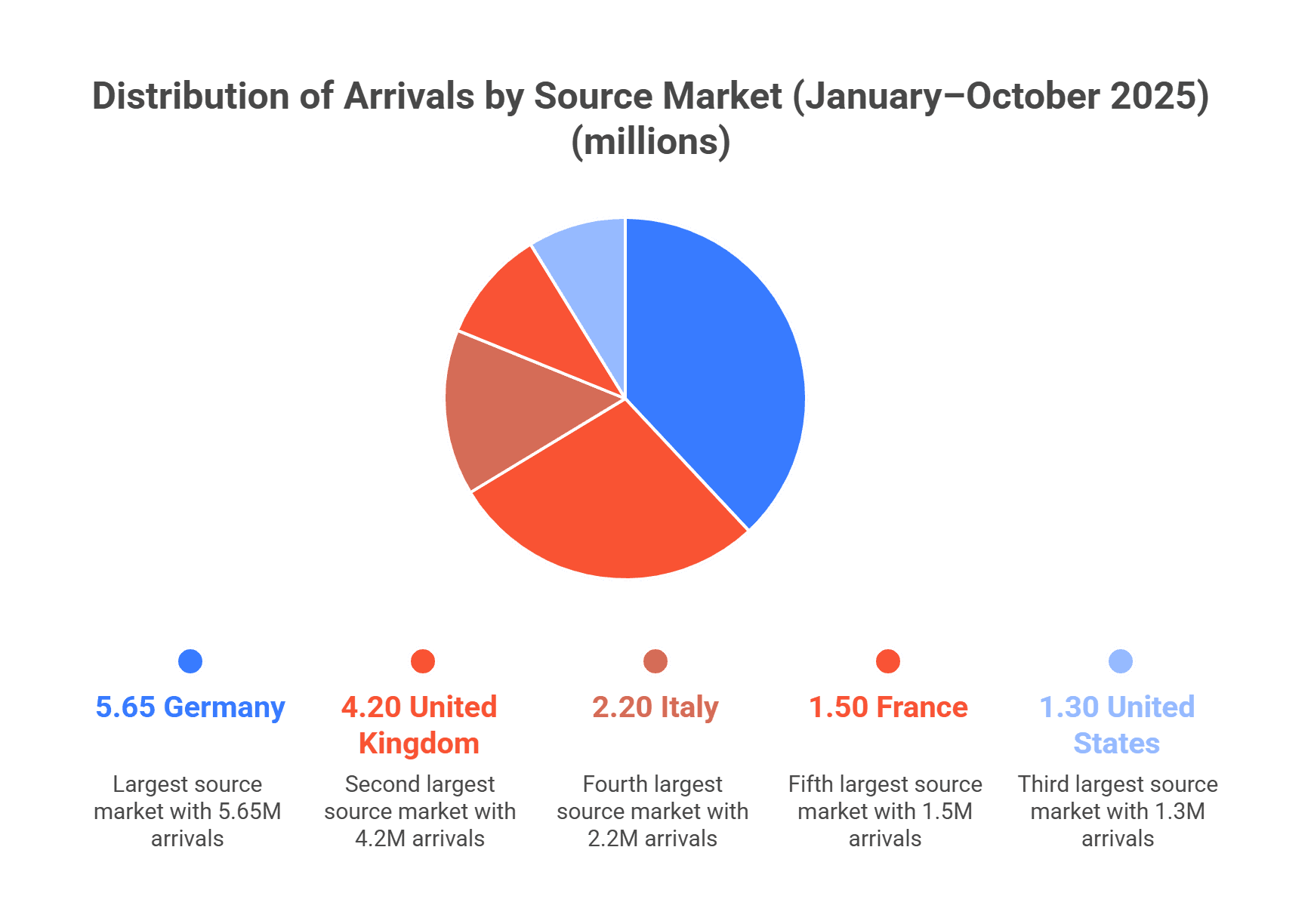

Germany held its position as Greece's largest source market in 2025, delivering 5.65 million arrivals (+8.3%) and €3.61 billion in receipts through October. But Germany's revenue growth was nearly flat at just 0.5% — volume is growing, yield is not. The September data was particularly stark: German receipts fell 28.3% that month alone, suggesting price sensitivity among eurozone travelers as the European economy cooled.

The United Kingdom told a different story entirely. UK receipts reached €3.55 billion through October, a 15.1% surge that dramatically narrowed the gap with Germany. October was especially striking, with UK spending up 42.9% year-over-year — an outlier driven by strong late-season demand for Greek islands and an increasingly favorable Sterling-to-Euro exchange rate.

The United States continued its trajectory as Greece's most valuable per-capita market, with receipts reaching €1.54 billion (+8.4%). Italy and France rounded out the top five at €1.27 billion and €1.02 billion respectively. France was the only major market to show an arrival decline (-2.0%), though French visitors still managed to increase their spending.

Non-EU markets collectively grew 12.2% in revenue versus 5.8% for EU sources — a divergence that reflects both the higher spending power of long-haul travelers and the softening of eurozone consumer confidence. For the Greek tourism industry, the strategic implication is clear: diversifying beyond traditional European markets isn't just prudent, it's increasingly where the growth is.

Airport traffic: 83 million passengers and Crete's milestone

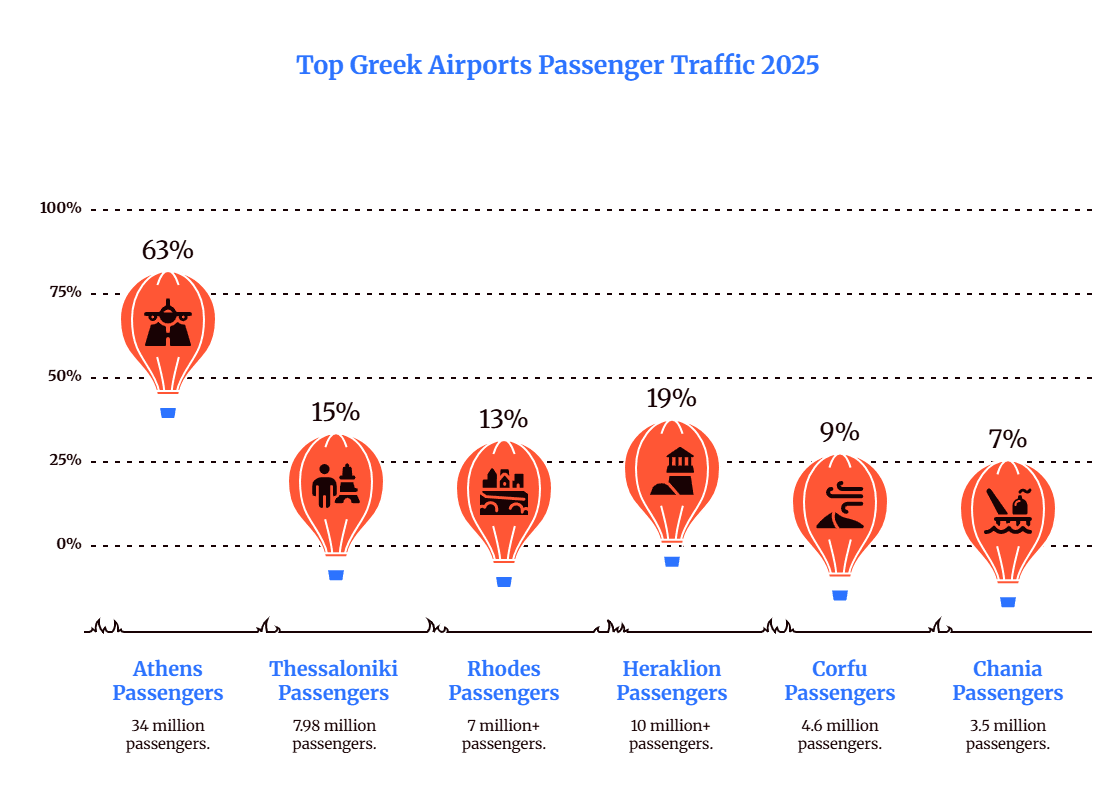

Greece's 39 airports handled a combined 83.33 million passengers in 2025, a 4.9% increase over 2024. The traffic distributed across three operators, each with its own growth story.

Athens International Airport achieved a record 34 million passengers, with international traffic surging 8.6% to reach 24.36 million. The capital's performance reflects a broader trend: Athens is increasingly functioning as a destination in its own right, not merely as a gateway to the islands. December alone processed 2.31 million passengers (+8.4%), and Athens ranked third among European mega-airports for November growth at 9.6%.

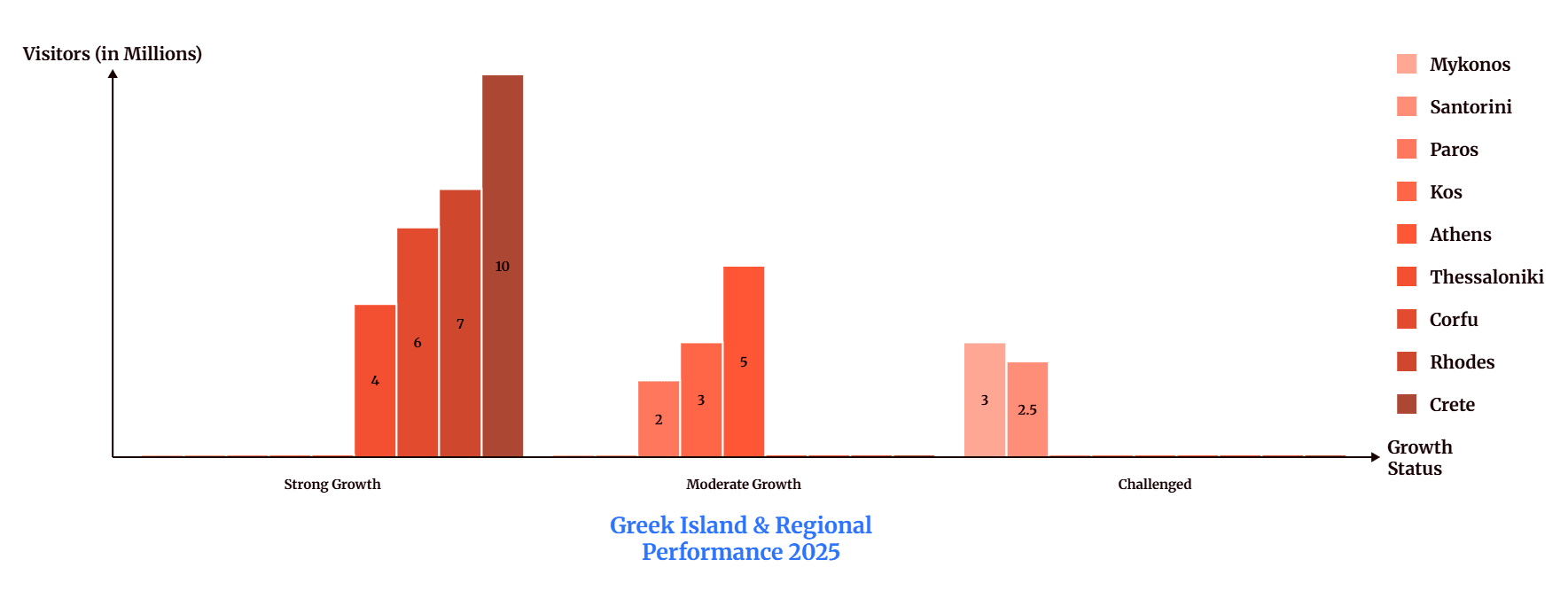

Fraport Greece's 14 regional airports served 37.12 million passengers (+3.0%), reaching 48% growth since the 2016 pre-concession baseline. Thessaloniki was the network's strongest performer at 7.98 million (+8.2%), while Rhodes exceeded 7 million passengers for the first time. August 2025 set a single-month network record of 6.8 million passengers.

But the most significant milestone belonged to Crete. Heraklion Airport surpassed 10 million passengers for the first time in its history, with international arrivals up 6.5% and domestic traffic rising 10%. Perhaps most remarkably, December international traffic at Heraklion surged 208% year-over-year — a figure that speaks to Crete's rapidly evolving identity as a genuine year-round destination. Chania Airport grew 6.7% in August, adding to the island's momentum.

A tale of two islands: Crete's record vs. Santorini's reset

No single comparison captures the shifting geography of Greek tourism more clearly than the divergent fortunes of Crete and Santorini in 2025.

Crete's Heraklion Airport crossed the 10-million passenger threshold with international arrivals up 6.5% and domestic traffic surging 10%. The island's cruise ports posted strong gains too: Chania broke its all-time record with 401,530 cruise passengers (+40%) across 204 calls — the port's best performance since cruise activity began in 2011. The JW Marriott's opening in Chania — Marriott's first Greek property — signals the kind of institutional confidence that tends to accelerate further investment.

Santorini, by contrast, experienced its most challenging year in recent memory. Air arrivals fell 19.1% in the first half of 2025, with the full-year projection at 3.18 million passengers — a 16.1% decline. The causes were compounding: a February earthquake sequence (magnitudes up to 5.3) triggered widespread booking cancellations, airline seat capacity dropped 26%, and the new daily cruise passenger cap of 8,000 reduced peak-day volumes by 27%.

Hotel occupancy on Santorini fell to 70% in June 2025 — down from 85% the previous June — and accommodation revenue declined 22% in the first half of the year. The island's tourism economy contracted by more than a fifth even as national figures hit all-time highs.

Yet the picture isn't entirely negative. Luxury properties like Canaves Ena reported slight increases, suggesting the high end of the market remains resilient. Visitor experience improved with reduced crowds, and the municipality launched "Santorini 2025: Year of Promoting and Supporting Authenticity" to reposition the island's brand. Over 100 properties now stay open through winter, a meaningful shift from the near-total seasonal shutdown that characterized Santorini as recently as 2018.

For travelers deciding which Greek island to visit, the divergence offers a practical insight: Santorini's lower occupancy means better availability and potentially sharper pricing, while Crete's infrastructure expansion — including the new Kastelli airport opening in 2027 — suggests it can absorb growing demand without the congestion that has begun to diminish the Santorini experience.

Other island performance: Rhodes recovers, Corfu extends, Mykonos pauses

Beyond the Crete-Santorini divergence, individual island performance in 2025 revealed important patterns.

Rhodes completed its recovery from the devastating 2023 wildfires, exceeding 7 million passengers with August achieving a historic milestone: 1.3 million passengers in a single month — a first for any Fraport regional airport. The Israeli market surged 42.9% in August, adding a new high-value source to an island traditionally dominated by British and German travelers.

Corfu projected more than 4.6 million passengers (+6%), with November showing exceptional 25.5% growth — evidence that the Ionian island is successfully extending its season beyond summer. Q2 accommodation revenue rose 10.7%, and a terminal expansion is underway to absorb continued growth.

Mykonos traffic remained essentially flat, with May 2025 at 128,289 passengers (+1.29%). The island faces a more immediate challenge: runway reconstruction closed the airport from mid-November 2025 through mid-March 2026. Combined with the €20 peak-season cruise passenger fee, Mykonos is navigating capacity constraints that may permanently alter its seasonal rhythm.

Thessaloniki, increasingly positioned as northern Greece's cultural and gastronomic gateway, achieved full-year growth exceeding 8%, with international arrivals growth of 10.7% leading all Greek airports in the first half.

Cruise tourism: caps, taxes, and port diversification

Greece's cruise sector generated €1.1 billion in receipts in 2024, a 22.4% year-over-year increase, with 7.8 million cruise passenger visits across an estimated 5 million individual travelers. The 2025 season built on this momentum while introducing significant regulatory changes.

Piraeus achieved a record 1.85 million cruise passengers with 863 ship calls, and more than 1 million passengers homeported from the port — embarking or disembarking cruises in Athens rather than simply docking for a day visit. This homeporting trend strengthens Athens' position as a cruise origin point and generates higher economic impact than transit calls.

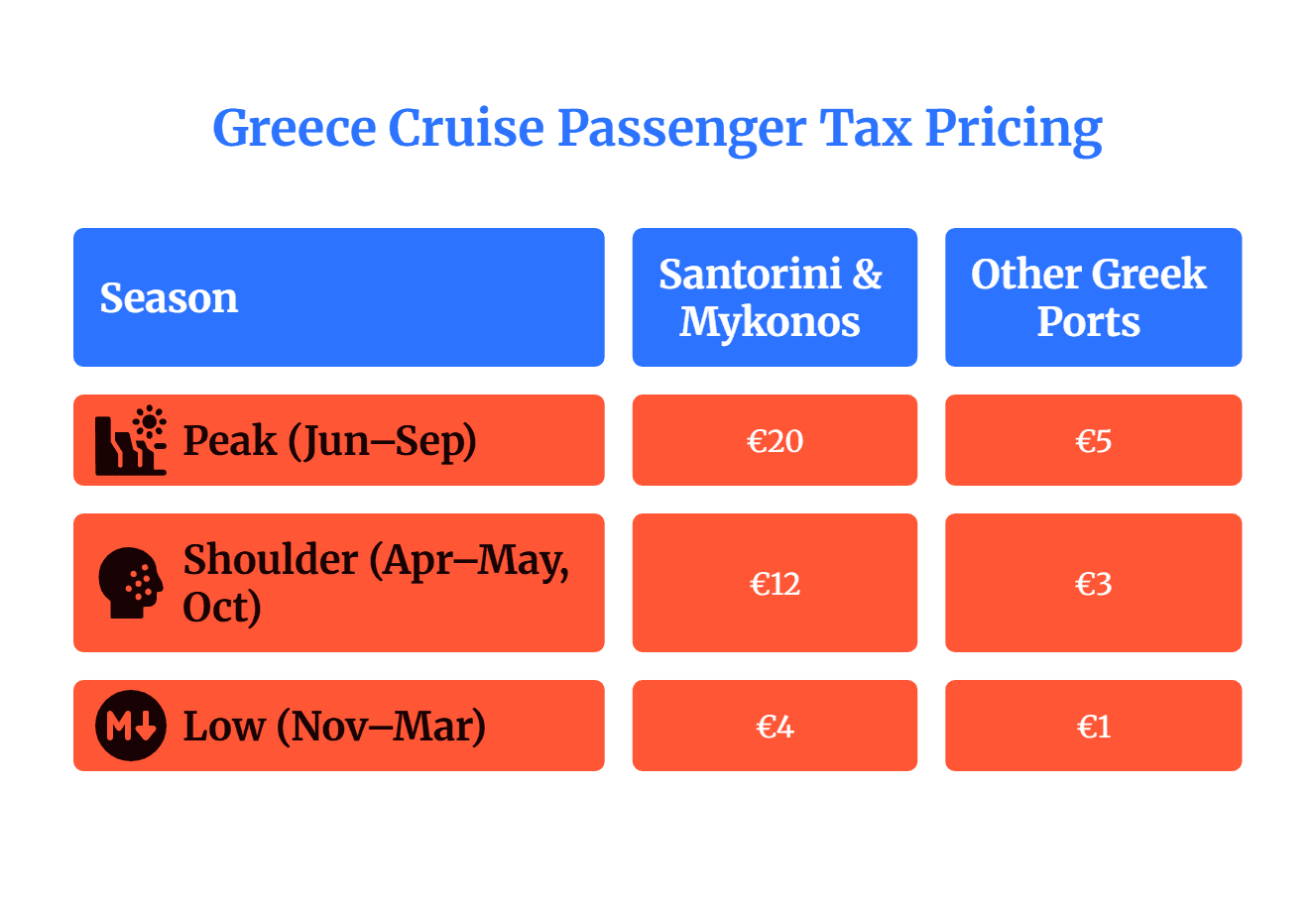

The most significant development was Santorini's daily cruise cap of 8,000 passengers, a 27% reduction from peak days that previously saw 11,000 to 17,000 passengers flooding the caldera villages. The cap operates through a scoring algorithm that rewards cruise lines for longer calls, off-season visits, and reliable scheduling. Penalties of €3 per passenger for late cancellations and €2 per passenger for early departures enforce compliance.

Early results include a 15% reduction in water consumption during regulated periods and significantly reduced cable car queues — previously one to two hours — suggesting the cap is delivering its intended quality-of-life improvements.

Greece also implemented a tiered Sustainable Tourism Fee on cruise passengers in July 2025. The structure creates powerful financial incentives for seasonal and geographic redistribution:

The fee is projected to generate €45–55 million annually, split among local municipalities (one-third), the Ministry of Maritime Affairs (one-third), and the Ministry of Tourism (one-third).

The combined effect of caps and taxes is already visible in cruise line behavior. Norwegian Cruise Line dropped Corfu and modified Mykonos timings. Meanwhile, alternative ports are capitalizing: Chania broke its all-time cruise record (+40%), Corfu has confirmed over 500 calls for 2026, and Thessaloniki expects 20 different cruise ships from 14 companies in 2026 — with 10 ships visiting for the first time.

The new cost of visiting Greece: accommodation taxes explained

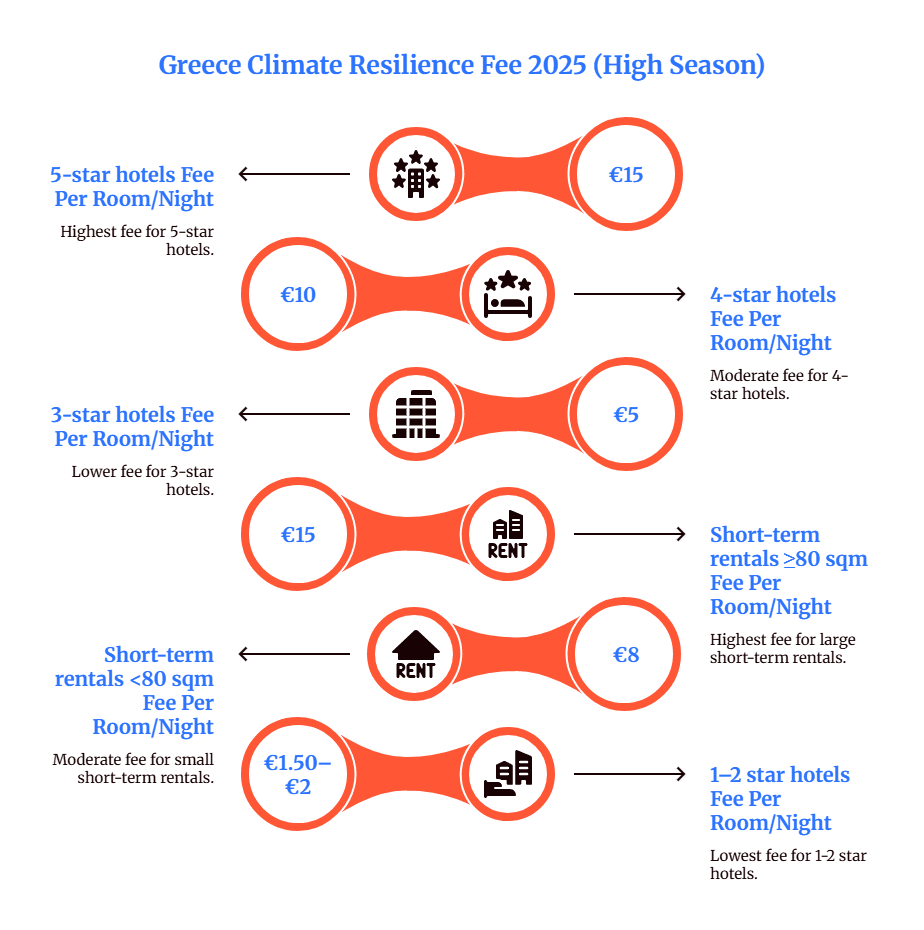

Alongside cruise fees, Greece increased its Climate Resilience Fee on overnight accommodation effective January 1, 2025. The levy — which replaced the prior stay-over tax — affects every visitor who books a hotel room or short-term rental.

The fee generated €368.92 million in 2024 — a 149.6% increase over 2023 — and exceeded Ministry of Finance projections by €167 million. The 2025 projection is approximately €570 million. Funds are dedicated to disaster preparedness and climate adaptation, a response to the devastating 2023 wildfires and floods.

In practical terms, the fee adds €140–210 per week to a 4- or 5-star hotel stay during peak season. For travelers weighing the total cost of a Greece trip, the new tax structure creates a genuine financial incentive to visit during November through March, when fees drop to as little as €3 per night at a 4-star hotel. It also narrows the price gap between short-term rentals and hotels, since larger rental properties now face the same €15/night levy as 5-star properties.

Hotel market: Athens strengthens, Santorini recalibrates

Athens hotels achieved 77.1% occupancy in 2025, up 0.9 percentage points year-over-year, with average daily rate (ADR) at €177 and revenue per available room (RevPAR) at €137. The city's most encouraging signal came from off-peak performance: occupancy during the January–March and November–December periods rose 5.3%, with ADR up 5.4%. Peak-season occupancy actually dipped slightly (-1.2%), but higher rates more than compensated.

Athens is increasingly functioning as a year-round destination, not merely a shoulder-season gateway to the islands.

Thessaloniki outperformed in the first half with occupancy up 4.3%, ADR rising 4.4%, and RevPAR growing 5.4% — metrics driven by the city's 10.7% growth in international airport arrivals, the highest increase among all Greek airports.

Resort hotels nationally showed a pattern consistent with the broader premiumization trend: occupancy was roughly flat (-1.1% through June), but Total Revenue Per Occupied Room rose 8.9%. Hotels are earning more per guest even when rooms aren't filling faster.

The 2025 luxury hotel pipeline underscored international brand confidence in Greece. JW Marriott opened its first Greek property in Chania, Four Seasons launched on Mykonos (94 rooms, €78.6 million investment), and the former Hilton Athens began its transformation into The Ilisian complex, anchored by a Conrad Athens — the brand's first in Greece, with an estimated €1.25 billion economic impact over five years. Those considering a luxury trip to Greece now have meaningfully more ultra-premium options than even two years ago.

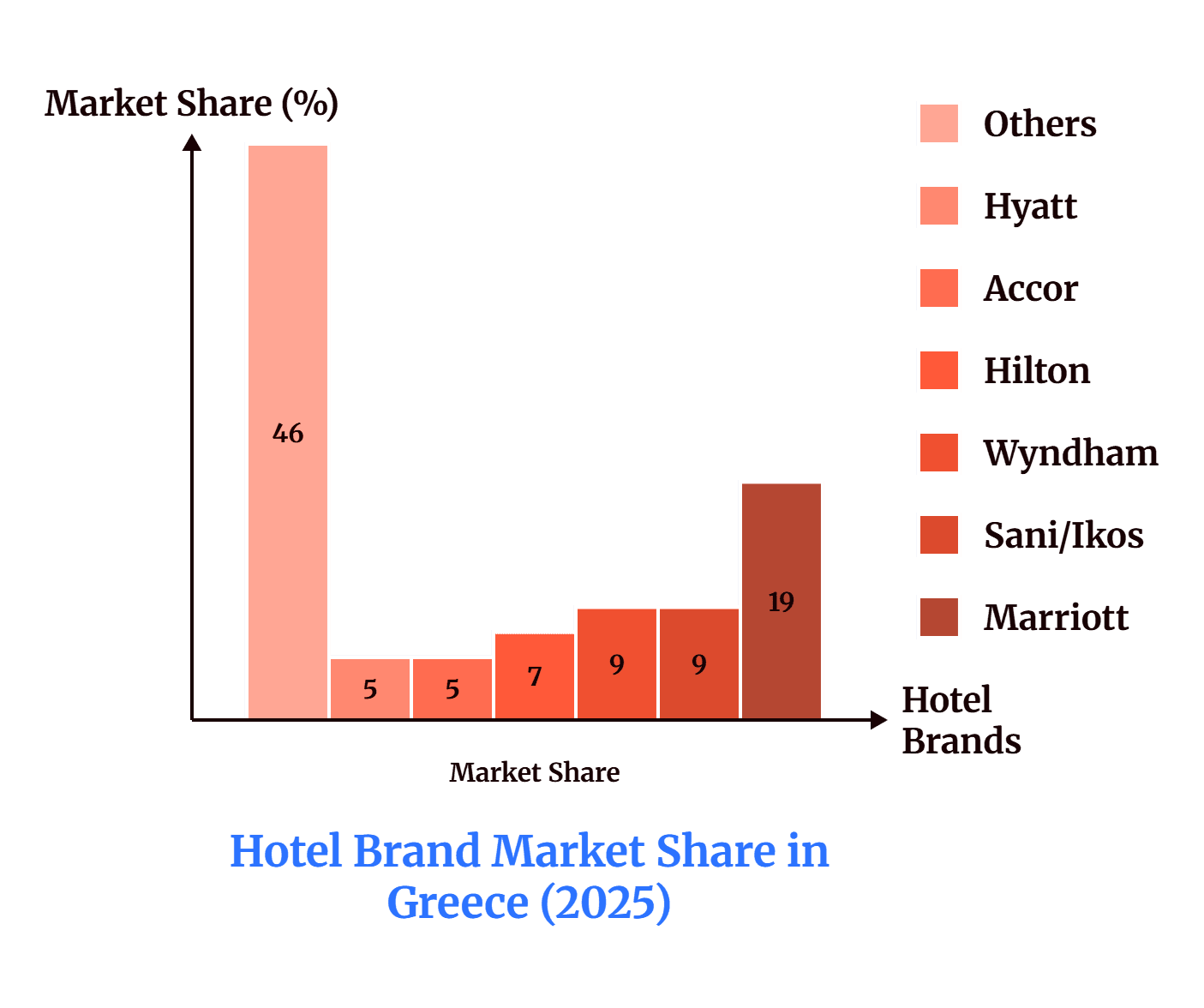

Globally, international chains operate 205 hotels with 29,204 rooms across Greece. Marriott leads with 19% market share (33 hotels), followed by Sani/Ikos (9%), Wyndham (9%), Hilton (7%), Accor (5%), and Hyatt (5%).

Short-term rentals: booming demand meets tighter regulation

Greece had 245,944 available short-term rental properties in July 2025, offering 1.078 million beds — 57,000 more beds than the same month in 2024. Athens alone accounts for 10,864 to 18,474 active listings, depending on the measurement methodology.

Demand is outpacing supply growth. AirDNA data shows Greece summer bookings (June–August) increased 22% year-over-year, ranking seventh in Europe. July 2025 supply grew 5% while demand grew 7.5%, lifting average occupancy by two percentage points to 51%. Athens listings achieved 71% average occupancy with ADR of €80–115.

But the regulatory environment is tightening significantly. Law 5170/2025, effective October 1, 2025, imposed new requirements: mandatory safety standards including smoke detectors, fire extinguishers, and liability insurance; a ban on basement and semi-basement units; and a limit of two properties per individual, with three or more requiring formal business registration. Fines range from €5,000 to €20,000 for violations.

Most consequentially, Athens' central districts banned new short-term rental registrations through 2026, with expected expansion to Thessaloniki, Halkidiki, Santorini, Paros, and Chania.

Shoulder season: October through December proves viable

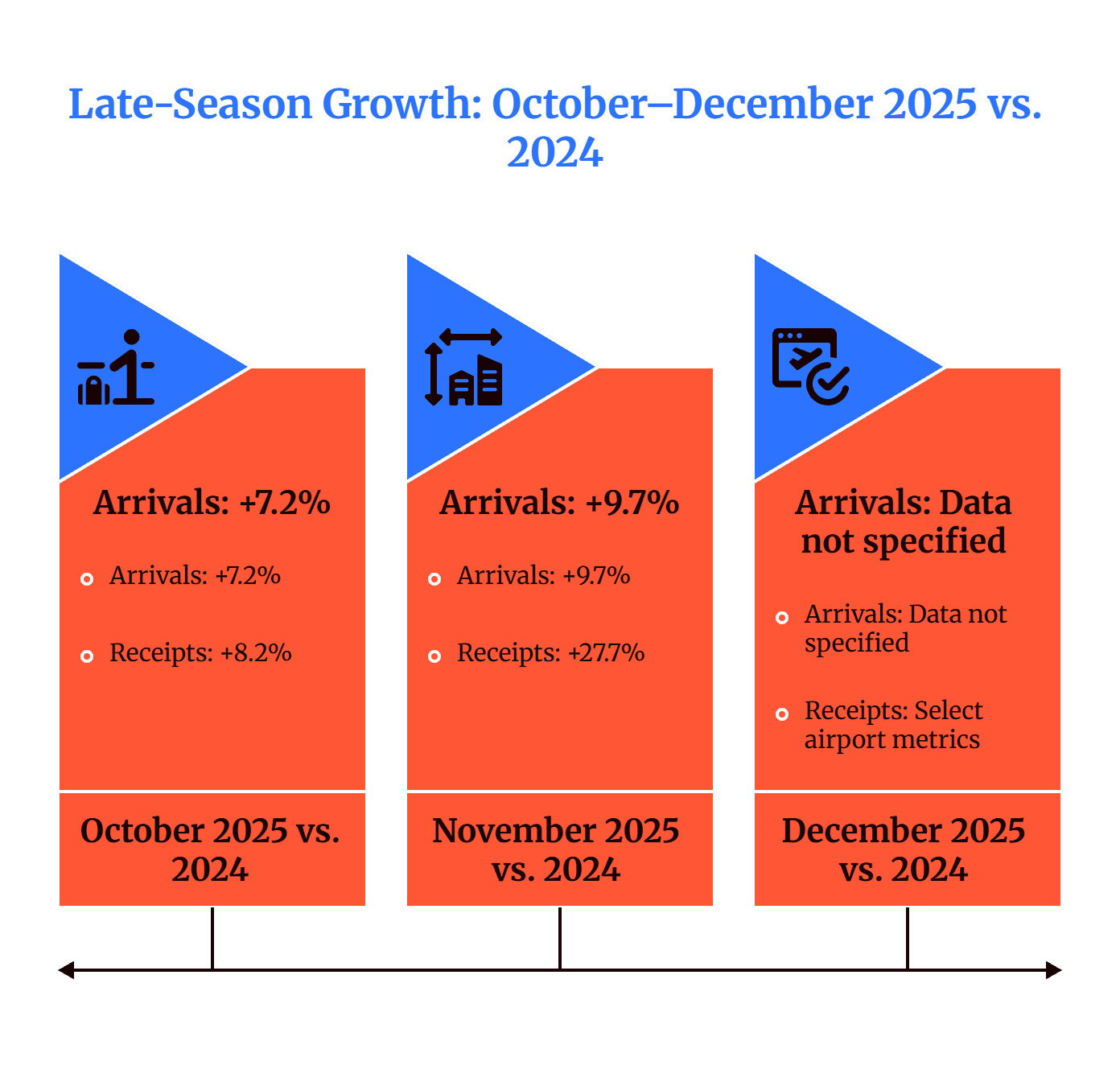

The data from late 2025 makes a compelling case that Greek tourism's seasonal boundaries are genuinely expanding.

October delivered 3.66 million arrivals (+7.2%) generating €2.25 billion in receipts (+8.2%). UK receipts surged 42.9% in October alone, with Italy up 31.7% and Germany up 9.8%. November travel receipts rose 27.7%, while visitor arrivals increased 9.7%.

December airport data reinforced the trend: Heraklion international traffic surged 208%, Thessaloniki grew 10.7%, Rhodes rose 8.4%, and the Fraport regional network expanded 9.4%. Athens off-peak hotel performance saw occupancy rise 5.3% with ADR up 5.4%.

Santorini now keeps more than 100 properties open through winter. Crete, Thessaloniki, and Athens function as genuine year-round destinations. The Tourism Ministry is actively promoting Epirus mountain tourism and mainland cultural heritage for winter visitors.

For travelers, the shoulder-season value proposition is increasingly hard to ignore. The Climate Resilience Fee drops by 60–80% outside peak season. Cruise taxes fall to €1–4 at most ports. Hotel pricing softens while weather in October — and often well into November — remains warm enough for swimming on most Greek islands. Our 10-day Greece itinerary guide works particularly well when adjusted for shoulder-season timing.

Tourism employment: growth constrained by labor shortage

Greece employed 401,000 workers in tourism in 2024, a 4.8% increase over 2023, with peak Q3 employment reaching a record 451,400. Including indirect effects — suppliers, transportation, food production — the World Travel & Tourism Council estimates tourism supports nearly 900,000 jobs, representing roughly 20% of all employment in Greece.

The industry faces a critical bottleneck: an estimated 80,000-worker shortage in hotels and food service, part of a broader economy-wide gap of 300,000+ foreign workers. Only about 25% of required workers have been recruited.

The government has responded with bilateral labor agreements with India (targeting 50,000 workers), Egypt, Vietnam, Bangladesh, Georgia, and Moldova. WTTC projects Greece could face 290,000 unfilled tourism positions by 2035 — a gap representing 27% of total sector demand.

For visitors, labor constraints manifest in subtle ways: reduced restaurant hours, slower service during peak periods, and occasional property closures. Solo travelers and couples visiting outside peak season are less likely to encounter these frictions.

Digital nomads: Greece's quiet growth market

One slice of Greece's visitor economy doesn't show up in arrival counts: remote workers who stay for months, not days. Since launching its Digital Nomad Visa in 2021, Greece has positioned itself as one of Europe's more aggressive competitors for long-stay, high-spend professionals — the opposite end of the spectrum from the shortening 4.7-night average trip.

Why Greece is competing for them

The economic logic mirrors the wider 2025 trend toward value over volume. A nomad on the €3,500/month threshold spends across a full quarter or more — accommodation, dining, co-working, domestic travel — concentrated heavily in the shoulder and off-seasons that Greece is working hard to fill. The 50% income-tax incentive, one of the more generous in the EU, is explicitly a "brain-gain" tool aimed at retaining skilled spenders rather than competing with the local labour market (visa holders cannot work for Greek-registered employers). Athens has since become a fixture on "best cities for remote work" lists, with Crete, Syros and Thessaloniki emerging as lower-cost alternatives.

What the data actually shows — and what it doesn't

Here the honest answer matters: Greece does not publish an authoritative annual count of digital-nomad visa holders. Figures circulating online — claims of tens of thousands of participants or billion-euro contributions — originate almost entirely from immigration-service marketing pages, not Bank of Greece or Ministry of Migration statistics, and should be treated with caution.

What is documented is the program's framework, its growing application volume (which prompted stricter income and documentation enforcement in 2025), and the policy intent. Until official figures are released, the responsible read is directional: demand is rising and Greece is investing in capturing it — but the precise headcount is not yet a published statistic.

Investment pipeline: €12 billion since 2022

The capital flowing into Greek tourism infrastructure over the past three years has been extraordinary. Approximately €12 billion has been invested in Greek tourism since 2022, with 700+ hotels opened or refurbished and 450+ new 4- and 5-star properties launched since 2019.

Three major strategic investments totaling €1.2+ billion were approved in March 2025 alone: Hydra Rock sustainable resort in Peloponnese (€474 million), GH Hotel eco-resort in Evia (€224 million), and an Astakos mega-yacht marina (€524 million).

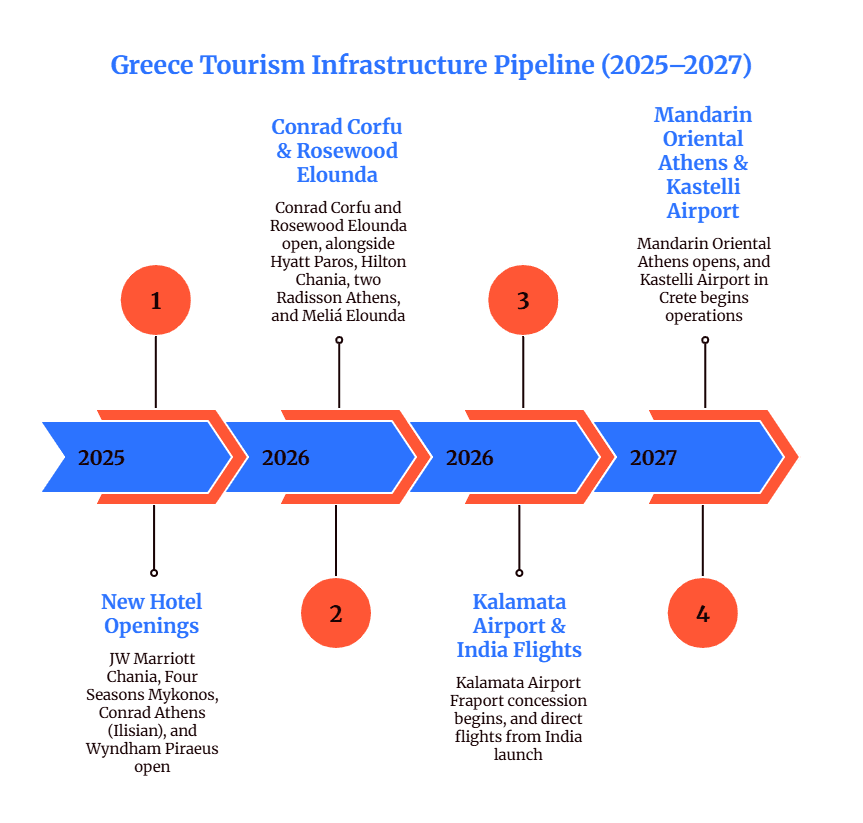

The hotel pipeline for 2026–2027 reads like a global luxury directory:

Confirmed 2026 openings include Conrad Corfu (136 rooms), Hilton Chania Old Town Resort & Spa (85 rooms), Rosewood Blue Palace in Elounda — the first Rosewood in Greece — Radisson Theatrou Square in Athens (173 rooms), Destination by Hyatt Paros (50 rooms, the brand's first in Greece), and INNSiDE by Meliá Elounda (86 rooms, Meliá's first Greek property).

2027 brings the Mandarin Oriental Athens (123 rooms plus 17 residences), further elevating the capital's ultra-luxury positioning.

In total, 60+ hotel projects worth billions of euros are expected to open by 2027. Hilton plans 18 total properties in Greece; Accor intends to double its eight-property portfolio.

New routes opening Greece to new markets

The 2026 airline schedule brings potentially transformative connectivity changes.

The most significant: India receives its first-ever direct connections to Greece. IndiGo will operate Delhi–Athens and Mumbai–Athens three times weekly each from January 2026, while Aegean launches Athens–Delhi (five times weekly from March) and Athens–Mumbai (three times weekly from May). Combined, 14 weekly frequencies will connect Athens to a market of 1.4 billion people — a source market Greece has barely tapped.

From the United States, American Airlines adds Dallas Fort Worth–Athens starting May 2026, while United continues Washington Dulles–Athens with upgraded aircraft. These complement existing services and deepen US market access beyond the traditional New York and Philadelphia gateways.

In Europe, Jet2's decision to open a London Gatwick base serving 10 Greek destinations is particularly consequential for the UK market. The carrier is adding 30,000 extra seats and will offer 360+ weekly peak departures, with new routes to Samos, Olympus Riviera (Pieria), and Meganisi. Finnair adds Helsinki connections to Thessaloniki, Kos, and Lemnos.

Aegean's fleet expansion includes two A321neo XLR aircraft with 138 seats and 24 lie-flat business-class seats, enabling potential new long-haul destinations including Bangalore, Seychelles, Maldives, and Nairobi.

Climate and sustainability: the long-term backdrop

Research projects mean temperature increases of +2.5°C (up to +3.8°C in summer) for Greece by 2046–2065 versus 1961–1990 baselines. Heat wave days are expected to increase by 15–20 annually by 2050. By century's end, Greece may experience 50+ "tropical days" — above 35°C during the day, above 20°C at night — per year.

The tourism implications cut both ways. Shoulder seasons will likely become more attractive as traditional peak months grow uncomfortably hot, potentially accelerating the seasonal redistribution already visible in the data. April–May and September–October are becoming the sweet spot for weather-sensitive travelers, a trend our guide to first-time Greek island visits increasingly reflects.

On the risk side, Greece ranks as the fourth most vulnerable EU country for coastal erosion, with potential coastal retreat of 280+ meters by 2100. Wildfire risk increases 40%+ even under the Paris Agreement's 1.5°C target. Studies estimate a potential €825 million loss from reduced overnight stays under a +2.5°C warming scenario.

The new Climate Resilience Fee — projected to generate €570 million in 2025 — represents Greece's primary financial instrument for adaptation. Whether that revenue is deployed effectively toward infrastructure resilience will be a defining question for the next decade of Greek tourism.

Looking ahead: 50 million visitors by 2030?

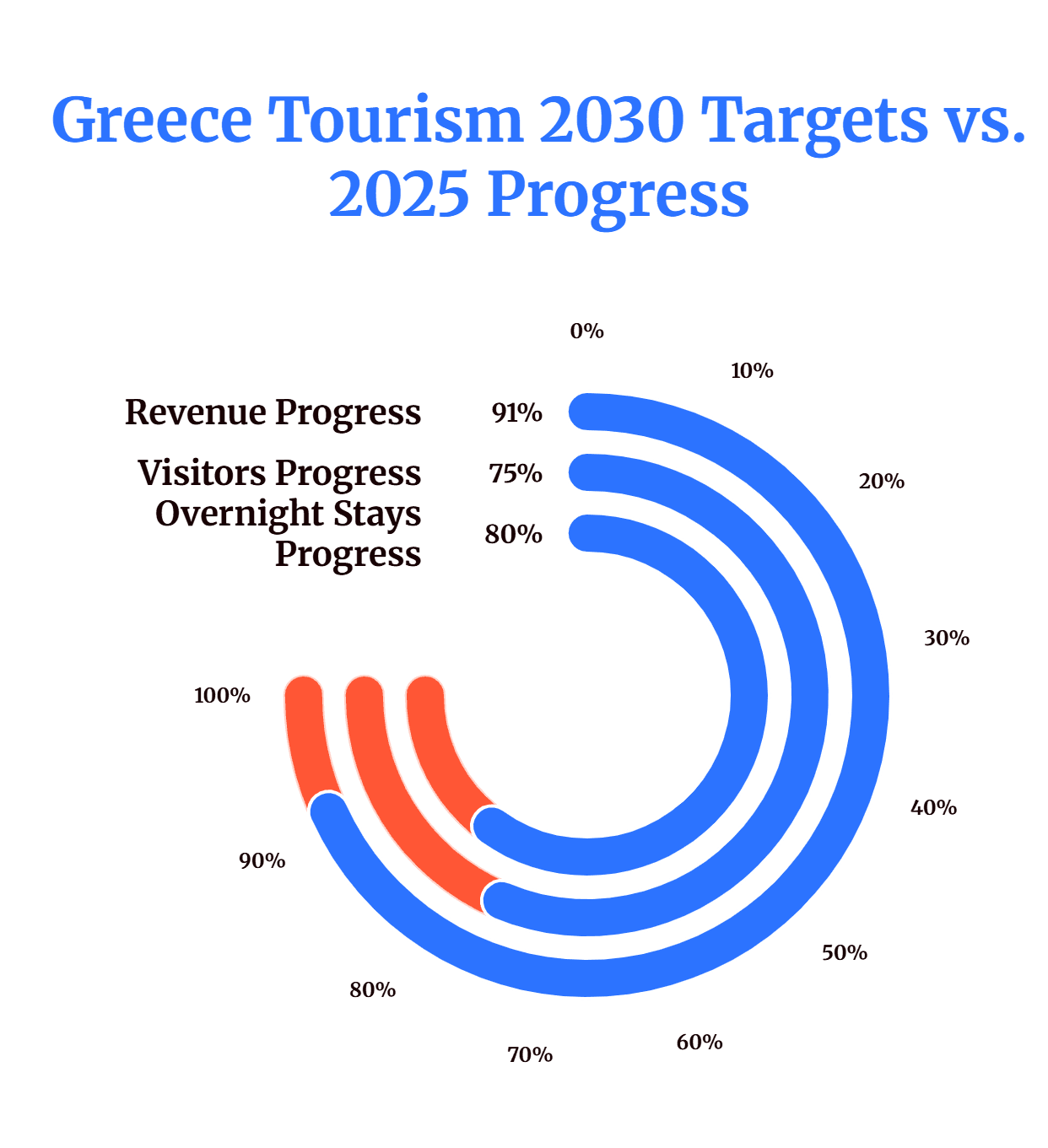

Greece's National Tourism Strategy 2030 sets ambitious targets: €27 billion in annual revenue (+52% versus 2019), 50 million annual visitors (+27% versus 2019), and 307 million overnight stays. Achieving these figures requires sustained annual growth rates of 6.2% in revenue, 3.5% in visits, and 4% in overnight stays through 2030.

From 2025's trajectory, the revenue target appears achievable — Greece is already more than 80% of the way there. The visitor target implies adding roughly 15 million annual arrivals over five years, a 40% increase that will depend heavily on infrastructure expansion (Kastelli, Athens airport upgrade, Kalamata concession) and new source markets (India, expanded US and UK connectivity).

Athens International Airport's €1.28 billion expansion targeting 40 million passenger capacity by 2032 — with Phase 1 construction beginning summer 2026 — provides the gateway infrastructure to support this growth. The new Kastelli airport in Crete, at 65% completion and targeting a February 2027 opening, will offer initial capacity of 10 million passengers expandable to 18 million, effectively doubling Crete's air access capacity.

The WTTC projects Greece's tourism GDP contribution to grow to €57.2 billion by 2033–2034, representing 23.6% of the national economy — roughly one in four euros generated in Greece flowing from tourism and its supply chain. Total employment contribution is expected to exceed 1 million jobs by 2034.

Methodology and data sources

This analysis draws on official data from the Bank of Greece (travel receipts, arrivals, and expenditure surveys), INSETE statistical bulletins (airport traffic, regional breakdowns), Athens International Airport and Fraport Greece traffic reports, individual port authority records (Piraeus, Corfu, Heraklion, Chania, Mykonos), and the World Travel & Tourism Council's economic impact assessments. Hotel performance metrics are sourced from STR Global and GBR Consulting reports. Where full-year 2025 data is not yet available, the analysis uses January–October or January–November figures as specified, and notes projections where applicable.

All currency figures are in euros unless otherwise stated. Arrival figures exclude cruise passengers unless specifically noted. Revenue figures from the Bank of Greece include cruise receipts in the total (€22.38 billion) but report the non-cruise component (approximately €20.6 billion for 2024) separately where available.

Plan your 2026 Greece trip

The 2025 numbers show where Greek tourism is heading — record arrivals, shifting source markets, and growing island traffic. To translate that into your own trip, start with our worked example of a 7-day Greece itinerary, then consider the realistic cost of a trip to Greece and if Greece is expensive by European standards.

Choosing islands is where most travelers get stuck. Our head-to-head guides cover Corfu vs Crete, Corfu vs Zakynthos, Naxos vs Paros vs Milos, Naxos vs Santorini, Naxos vs Crete, Paros vs Santorini, and Paros vs Mykonos. If your time is limited, the best Greek islands near Athens are reachable as quick escapes from the capital.

Once you've picked your destinations, we cover where to stay in Naxos, the best hotels in Paros, top hotels in Mykonos, and top hotels in Milos. For dining, our restaurant guides for Santorini, Mykonos, Heraklion, Chania, Rethymno, and Skiathos cover Greece's main food destinations.

For getting there, see our overview of direct flight routes to Greece and our dedicated guide on flying to Greece from the USA.

Data Sources

Data period: 2024–2025 (with 2019 baseline)

Methodology

This analysis draws on official data from the Bank of Greece (travel receipts, arrivals, and expenditure surveys), INSETE statistical bulletins (airport traffic, regional breakdowns), Athens International Airport and Fraport Greece traffic reports, individual port authority records (Piraeus, Corfu, Heraklion, Chania, Mykonos), and the World Travel & Tourism Council's economic impact assessments. Hotel performance metrics are sourced from STR Global and GBR Consulting reports. Where full-year 2025 data is not yet available, the analysis uses January–October or January–November figures as specified, and notes projections where applicable. This analysis synthesizes official statistical releases with industry reporting to present a comprehensive view of Greece's tourism performance. Where sources report slightly different figures (e.g., total arrivals including vs. excluding cruise passengers), the distinction is noted. Projections use observed growth rates from available partial-year data applied to known seasonal patterns.

Tourism statistics are subject to revision as authorities finalize annual reports. The Bank of Greece adjusts preliminary monthly data in subsequent releases. Full-year 2025 data was not available at the time of publication; analysis uses the most recent partial-year data available (January–October or January–November 2025 as specified).

The Greek Trip Planner research team analyzes tourism data, government statistics, and industry reports to provide actionable insights for travelers and travel professionals.